Chapter 26 – Employment Responsibilities

26.1 Overview

Employing staff comes with a range of challenges, responsibilities and compliance requirements. It can also be the best thing you do to grow your business and achieve your objectives.

This section summarises key points to help you fulfil your obligations as a good employer, reduce day-to-day problems and comply with the law.

26.2.1 Employment Relations Act 2000 (ERA)

26.2.2 Employees vs Contractors

26.2.3 Employers and the IRD

26.3.1 Employment Agreement

26.3.2 Human Rights Act 1993

26.3.3 Harassment

26.3.4 Harmful Digital Communications Act (Cyber bullying)

26.3.5 Immigration Act 1987

26.3.6 Privacy Act 1993 (see also 25.8)

26.3.7 Employer Rights to Intellectual Property

26.3.8 Poor Performance

26.3.9 Disciplinary Process

26.3.10 Terminating Staff

26.3.11 Redundancy

26.3.12 Personal Grievance

26.4 Remuneration And Payment Issues

26.4.1 Minimum Wage

26.4.2 Registration

26.4.3 Deduction of PAYE

26.4.4 Employee Reimbursement

26.4.5 Reimbursement of Motor Vehicle Expenditure

26.4.6 Extra Pay and Emoluments

26.4.7 Holiday Pay

26.4.8 Shareholder Employees (ITA s EA 4)

26.4.9 Gifts, Tips or Gratuities

26.4.10 Inducement Payments

26.4.11 Restrictive Covenants

26.4.12 Damages and Compensation

26.4.13 Tax Free Employee Allowances

26.4.14 Other Matters

26.5 Kiwisaver Scheme

26.6 Contractors’ Schedular Payments

26.7 The 90-Day Trial Period

26.8 Holidays And Leave Entitlements

26.8.1 Statutory Holidays

26.8.2 Annual Holidays

26.8.3 Sick Leave

26.8.4 Bereavement Leave

26.8.5 Domestic Violence Victim Protection Act 2018

26.8.6 Parental Leave and Employment Protection Act 1987

26.9.1 Compliance

26.9.2 Rest and Meal Breaks

26.9.3 Infant Feeding

26.9.4 Other Health and Safety Issues

26.10 Drug Testing

26.11 Smoke Free Environments Act 1990

26.12 Volunteers Employment Protection Act

26.2 Application

26.2.1 Employment Relations Act 2000 (ERA)

New Zealand law recognises employment as a human relationship involving issues of mutual trust, confidence, consultation and fair dealing. Employers, employees and unions are all required to deal with each other in good faith and this principle underpins the ERA.

26.2.2 Employees vs Contractors

The type of relationship an organisation has with workers will affect the employer’s obligations. It is important to establish at the outset whether the person providing services to your business is an employee or alternatively an independent contractor. This will generally be a question of fact and law. Several tests have been developed for distinguishing between an employee and an independent contractor. The IRD has issued an interpretation statement, IG11/01: Income tax; goods and services tax – determining employment status for tax purposes (employee or independent contractor).

This sets out the following tests applied by the courts to determine whether a worker is an employee or contractor.

Intention: What is the true intention of the relationship? This can sometimes be established by the wording in the employment agreement. However, the agreement is unlikely to mask the true intended relationship and the courts will look deeper if the facts point to something different. The intention of the parties is relevant but no longer decisive. The norm within an industry can be taken into account when establishing the intention.

Control: This test considers the degree of control the employer exerts over the work and the manner in which it is to be done. The more the employer specifies work content, hours and methods, and the more the work can be supervised and regulated, the more likely the person engaged to do the work is an employee.

Independence: A contractor will typically have a greater degree of freedom to choose how the job will be done. The following are indicators of independence:

The person has multiple clients (but if the person works for only one client, this does not necessarily mean the person is an employee);

The person is free to work from their own premises;

They supply their own tools or equipment for the job;

They share in the risks;

They can hire or fire whomever they wish to help them do the job;

They advertise and invoice for the work;

They pay or account for taxes and government and professional levies.

Integration: Under this test, a job is likely to be done by an employee if it is:

integral to the business organisation and not merely an accessory to it;

the type of work commonly done by “employees”;

continuous (not a “one-off” or intermittent activity);

for the benefit of the business rather than for the benefit of the worker.

Fundamental: This is also sometimes described as the “business test” or the “economic reality test”. It establishes whether the person performing the services is operating a business and doing the work on their own account. Has the person invested in a business and can it be sold? An independent contractor usually agrees to be responsible for the quality and completion of the work. They cannot be “dismissed” like an employee, but the contract can be terminated if it is breached. Other Factors to consider include:

whether the type of business or the nature of the job justifies or requires using an independent contractor;

the behaviour of the parties before and after entering into the contract;

whether there is a time limit for completing a specific project;

who is responsible for correcting sub-standard work and

who is legally liable if the job goes wrong.

Employment law only applies to employees, affording them similar benefits as other employees. These include minimum wage rates, paid leave, and so on. An employee can take out a personal grievance for unfair treatment including dismissal. As the employer, you must deduct PAYE from their salary or wages.

A contractor is not entitled to these benefits, but can claim tax deductible business expenses and enjoy more flexibility.

Care should be taken to ensure that each worker is treated correctly according to the actual relationship to ensure that you meet your legal obligations.

Employees: The intention of the employee-employer relationship is to clearly form an ‘employment relationship’ and this is reflected in the employment agreement and/or behaviour of both parties.

Contractors: The intention of the parties to a contract is not to form an ‘employment relationship’ and this is reflected in the agreement and/or behaviour of both parties. If you hire sole-trading contractors, you must deduct withholding tax from their pay unless they hold an exemption certificate. See also Section 26.6. Invoices received from a registered company are not subject to a withholding tax deduction.

The employer/employee and contractor relationships are different and it is important to recognise that an employer cannot misconstrue an employee/employer relationship and treat it as hiring a contractor in order to avoid managing PAYE, paying holiday pay and Statutory Holiday pay, severance pays etc.

26.2.3 Employers and the IRD

Employers act as agents of Inland Revenue when making source deductions from monetary remuneration paid to employees or contractors. Severe penalties can apply for failure to comply with these obligations. Employers are also liable to account for deductions such as child support, student loan repayments and Court Fines on behalf of their employees.

In addition to these tax responsibilities, an employer takes on potential liabilities for sick pay, public holidays, annual leave, potential claims for unfair dismissal, and a few others beside!

26.3 Practical Issues

26.3.1 Employment Agreement

In practice, the employment relationship is established through an employment contract which may be a collective or individual agreement depending on the circumstances. Either way, the agreement must be established by good faith bargaining and must be in writing.

The employer must have a copy of the written agreement on file and available to provide to the employee on request. If your employee has not signed the agreement, you must keep a copy of the offered agreement on file, as it sets out the terms and conditions that apply. It is likely that there will be implied acceptance if the employee knows that these are the terms on offer, turns up to work and accepts the payment of salary or wages.

Through a written agreement both parties will have a clear understanding of their rights and obligations from the start of the relationship through to termination. The employment contract seals the agreement between the employer and employee and must be signed by both parties, each party retaining a copy.

A good employment agreement will cover all potential employment issues before these arise and through this medium there is a certain peace of mind for both parties. The key is to ensure both parties have a clear understanding of the employment relationship and their rights and obligations under it.

The contract must include not only the mandatory Clauses, but also those that are necessary under the circumstances to clarify all key matters and ensure that both parties are in full agreement.

Employment agreements must:

be in writing

name the employer and employee parties

describe the type of work to be performed

indicate where the work is to be performed

outline hours of work

state wages or salaries payable

contain a plain language explanation of the services available for the resolution of employment relationship problems (including reference to the 90-day limit for raising a personal grievance)

define details of annual leave, public holidays, sick and bereavement leave

describe how you will protect employees if the business is sold.

It may be advisable to add clauses covering:

probationary or trial periods (See 26.7)

an outline of employer and employee health and safety responsibilities

termination process (by either party)

redundancy process, provisions and payment details. (Note: Redundancy payments are not mandatory unless provided for in the agreement. Either way, it helps if the terms are agreed, documented and signed at the outset)

provisions to address specific issues such as protection of intellectual property (IP) including copyright; ability to test for alcohol and drugs, restraint of trade and so on.

The agreement should state that the employee has the right to seek independent legal advice prior to signing and reasonable time should be provided for this. Use our Q&A service if help is needed.

The employer is obligated to deduct PAYE, Child Support, KiwiSaver contributions and Student Loan monies from the employee’s pay including any other additional demands that may be made in writing by the Inland Revenue Department. Other monies may be deducted but this has to be agreed by the employee and should be signed off by the employee.

UNION RIGHTS AND COLLECTIVE BARGAINING

2018 Law changes strengthened workplace collective bargaining and union rights as follows:

Employers can no longer refuse to bargain for a Multi Employer Collective Agreement (MECA);

There is a duty to conclude bargaining unless there is a good reason not to;

There is no longer a process to declare bargaining over;

Unions are bound by timeframes in collective bargaining;

Employers must pass on information about unions to prospective employees with a form where the employee may choose to become a member;

Pay rates must be included in collective agreements and may include pay ranges or methods of calculation;

For the first 30 days, new employees must be employed under terms that are no less favourable than the collective agreement (30-day rule);

Employers must provide reasonable paid time for union delegates to represent other workers;

Employers may no longer deduct amounts from wages for low level industrial action;

• Union access is available without prior employer consent; and

• There are protections against discrimination for union membership and activities.

RESPONSIBILITIES

Every workplace and employer-employee relationship is different and it is difficult to elaborate too much on the above. Consultation with your legal advisor is recommended.

Mutual trust, respect and good faith are at the heart of employment relations and this is recognised by law as can be seen in the following sections.

26.3.2 Human Rights Act 1993

When hiring staff the employer must comply with specific criteria to ensure fair recruitment. An individual must not be unfairly prejudiced during the interview and hiring process. Employers must be aware of the following to avoid being liable.

The Human Rights Act sets out unlawful grounds for discrimination. In practice, it is recommended that businesses be run on the basis that discrimination for any reason whatsoever is not permitted. As an employer you cannot show preference for one person over another during engagement, appraisal, promotion, discipline or in your general dealings, based on any of the following:

sex

marital status

religion or beliefs

age

race, colour, creed, birth place

political opinion

employment status

sexual orientation

Also ensure when advertising, and in workplace forms and manuals, that you do not show any preference incorporating any of the above.

This Act applies in a number of situations, including employment, private superannuation entitlement, provision of goods and services, entry into places where the general public has access, and accommodation.

Businesses and particularly places of employment are advised to have written policies setting out what constitutes a breach of a human right, and what recourse is available. This policy document needs to be thorough from the point of view of protecting every individual, addressing the need for an effective complaints system, and allowing for cultural, language and religious differences.

26.3.3 Harassment

Harassment and how it will be dealt with should be detailed in your employment contract and/or policy and procedure manual. In the event of receiving a complaint, the employer should undertake an investigation into the alleged harassment in a procedurally fair manner.

Harassment may be in different forms as indicated below.

Sexual Harassment

Sexual harassment occurs when one employee makes continued, unwelcome sexual advances, requests for sexual favours, or other verbal or physical conduct of a sexual nature, to another employee, against his or her wishes.

Sexual harassment is treated severely by the Courts and contravenes the Human Rights Act. Examples include:

Smutty and sexual jokes

Language of a sexual connotation directed at somebody

Offensive hand or body language

Repetitive comments about somebody else’s sexual activities

Repetitive invitations to take somebody out when they continually object

Following somebody from the time they leave work

Unwarranted physical contact

Provocative posters or screen savers

Sexual assault or rape

If the accusation is of a serious nature it is advisable to involve the police immediately.

General Workplace Harassment

“…unwanted and unwarranted behaviour that a person finds offensive, intimidating or humiliating and is repeated, or significant enough as a single incident, to have a detrimental effect upon a person’s dignity, safety and well-being “.

Racial Harassment

Uninvited behaviour that humiliates offends or intimidates someone because of their race, colour, or ethnic or national origin. It can involve spoken, written or visual material or a physical act.

Bullying

There is no generally accepted definition, but bullying can include:

overt acts such as threats, intimidation, coercion, verbal abuse, shouting, unjustified criticism, unjustified threats of dismissal; and

covert behaviour such as deliberately overloading an employee with work, hiding tools and equipment, sabotaging an employee’s work, isolating or ignoring an employee.

26.3.4 Harmful Digital Communications Act (Cyber bullying)

It is a criminal offence under this Act (s 19) to post a digital communication with the intention of causing harm to a victim; if it does cause harm and would do so to an ordinary reasonable person in the position of the victim.

Proof that the communication is true will not be a complete defence, but may be taken into account by the Court along with the age of the victim and other factors.

26.3.5 Immigration Act 1987

You cannot continue to employ an individual if you are aware that they are working in New Zealand illegally. You can legally ask a job applicant whether they are a citizen, have a right of permanent residency in New Zealand or a work permit or limited purpose permit for working in New Zealand. Ask applicants to present evidence of their legal work status before employing them.

26.3.6 Privacy Act 1993 (see also 25.8)

The Privacy Act pertains to personal information about individuals. This includes information collected by employers about job applicants or employees and how this information is managed. For example, an employer cannot provide a reference on a former employee to another party without the consent (preferably in writing) of the former employee. It is advisable to obtain this consent as a matter of course in documentation signed at the time of hiring (preferably) or exit of the employee.

The decision regarding whether to employ an individual has to be made in a fair manner without bias or discrimination. The employer cannot request any information on matters listed in 6.3.2 above during interviews or on the job application form. Having agreed to employ an individual the employer can (and should) obtain personal information from the employee regarding age, sex, place of abode, telephone number, next of kin, etc. This may be required under a Health and Safety Policy to ensure safety of the employee and to support the employment relationship. The employer is privy to the employee’s personal information and this should not be released to any other party. It may only be used for the purpose for which it has been provided and should be retained only for as long as it is needed to satisfy that purpose.

If anybody calls to obtain personal details (such as a home address or telephone number) of a current or past employee you cannot legally divulge this information without permission from that employee. There are exceptions under special circumstances such as a notice (always ensure that it is in writing) from an authority that has the legal right to demand such information, e.g. IRD.

26.3.7 Employer Rights to Intellectual Property

Don’t assume you automatically own intellectual property that employees create.

In the absence of a written agreement, common law and equitable principles apply, and the question is whether the invention was made by the employee acting in the course of his or her employment. This is complex, but relates to

Nature and scope of employee’s duties.

Whether the invention was made during or outside working hours.

Whether the invention was conceived in the course of duties the employee was engaged to perform.

Whether the facilities or materials of the employer were used.

Even if the above tests are met, it does not necessarily follow that every invention by an employee is the property of the employer. For example, if sales managers are not expected to invent products, they may have a better claim to their inventions than the employer has.

The best way to protect yourself and your company is to have your expectations clearly expressed in the employment agreement. This would include appropriately drafted terms dealing with:

(1) Ownership of all employee-generated intellectual property.

(2) Assignment to the employer of such rights worldwide.

(3) Disclosure of all “inventive” ideas to the employer.

(4) Maintenance of adequate and current records of work done.

(5) The rights and obligations of the employee post termination.

The duties of the employee should be expressed as broadly as possible to increase the chances that any inventions made or works created by the employee are done so “in the course of employment”, but also be careful not to draft assignment or restraint clauses too broadly, making them unenforceable.

26.3.8 Poor Performance

Employee performance and behaviour can usually be improved through informal meetings. It is a manager’s role to speak to the employee, explain any concerns and work with the employee to reach agreement on goals and strategies to improve performance. Refer to specific examples where possible to demonstrate issues. Keep an open mind, There may be good reasons for the poor performance and these do not always relate to factors that are within the employee’s control. Ensure that the employee is clear about the expectations, concerns and consequences of failing to improve.

There may need to be a number of meetings like this to achieve the desired objectives but this approach is part of good management and often helps to bring out the best in the employee.

It is very important to keep a note of these discussions for future reference even though the meetings are informal.

However, if you don’t get the desired result, or the conduct continues then you may need to continue into a more formal disciplinary process.

The law does not spell out the procedure for managing poor performance. If the process includes the following, however, you will be able to demonstrate that you have been fair and complied with the principles contained in the ERA:

Provide the employee with written notice of the problem and advise the consequences of failing to remedy it.

The employer should make sure that the employee is aware of his or her rights which include being given:

an opportunity to respond to any concerns that are raised;

a fair hearing;

the option to have representation in any disciplinary meeting and time to arrange for this support; and

the right to appeal against disciplinary measures.

The employee must be given an opportunity to improve. This may involve the employer providing training.

The employer should take all other reasonable action to ensure that the employee can meet the employer’s expectations.

Only where an employee continually fails to meet specified standards for which that employee was engaged, and where suitable training has been provided in this regard, can the employer consider termination.

26.3.9 Disciplinary Process

Any disciplinary process followed must be procedurally fair. This will not necessarily stop an employee from filing a claim but if you find yourself in mediation or a court as an employer, you will at least be guarded against a charge of failing to follow due process.

26.3.10 Terminating Staff

It is advisable to address termination in your employment agreement. It is important to bear in mind that employers cannot terminate staff willy-nilly and that procedures need to be adhered to. Punitive damages for incorrect dismissal can be quite substantial.

An employee cannot necessarily be immediately terminated where he/she has not properly fulfilled his/her obligations. The employer accepted the responsibility of employing the employee and is therefore committed to that employee’s welfare. Accordingly, there is a process that must be adhered to in order for an employer to satisfy the minimum standards for procedural fairness.

The employer should have provided the employee with suitable written warnings and a final written warning before that employee can be terminated for failing to meet specified criteria. This process can take 1-9 months, depending on the nature of the work, in order to be fair to the employee.

An employee can be dismissed instantly for serious misconduct. However, a word of warning: firstly, this should be written into your employment contract, and secondly, serious misconduct may be viewed differently by another party (such as the Courts) to the way you may view it. Serious misconduct would generally involve an illegal act or failing to comply with the employer’s lawful instruction, failure of which could jeopardise the safety of others or severely compromise the employer’s business. The employer must have sufficient proof of serious misconduct in order to avoid substantial costs for improper dismissal.

In 2018, reinstatement was restored as the primary remedy for unfair dismissal. This means that the employee must be reemployed in the job. Due to the impact on relationships, however, the employee is likely to seek compensation rather than reinstatement.

In most industries the requirements about what happens to existing employees if the company they work for is sold, or their work is contracted out, will be set out in their employment agreement and is a matter between them and their current employer. The agreement must address what steps the employer will take for employees affected by any sale, transfer or contracting out of the business. Those agreements could range from spelling out explicitly the employee’s transfer and redundancy rights through to simply saying how these issues will be addressed at the time.

26.3.11 Redundancy

Employers are entitled to structure the business as they see fit to meet their commercial goals.

If a position becomes surplus to the requirements of the business, the employer must follow a fair process, consult the affected employees and consider all reasonable options and alternatives before making a final decision on redundancy. Where more than one person competes for a remaining position, the selection criteria should be fair and transparent. The employer must comply with the terms of the employment agreement relating to redundancy. A reasonable period of notice should be given.

The redundancy must be genuine. The reason for the position ceasing to exist should be apparent and make sense. An employer cannot use redundancy as an excuse to dismiss someone with poor performance and then employ someone new into the position. This is likely to give rise to a grievance claim on the grounds of unjustified dismissal.

A redundancy payment will normally be due only where this has been provided for in the employment (or subsequent) agreement. While there is no legal requirement to make a redundancy payment, the courts will look favourably upon an employer who does make a pay-out if an employee does take the matter to court.

An Exception for Vulnerable Workers

Part 6A of the ERA is designed to protect vulnerable workers. These are employees who provide cleaning, food catering, or laundry services. When a business is transferred, contracted out or sold, its vulnerable workers have a right to transfer to the new owner or operator of the business on the same terms and conditions and the outgoing employer is required to hand over information about the employees to the incoming employer. Such workers may decide decide whether they wish to transfer to the new employer or not. The outgoing employer must provide the new employer with a warranty that no steps have been taken that will damage the business of the new employer. For example, increasing employee entitlements before the transfer.

26.3.12 Personal Grievance

The law requires you to contain an explanation of the personal grievance procedure in your employment agreement.

A personal grievance may be brought against an employer for any number of reasons including:

Unjust dismissal, whether for redundancy, poor performance, serious misconduct, sickness or injury. The test here is whether the standard of a fair and reasonable employer has been met, taking the particular circumstances into account.

Unjustifiable and unfair amendments to employment conditions. This includes conditions that go past the end of the employment contract. Again, whether the employer’s actions were justifiable depends on the test of the “fair and reasonable employer”.

Discrimination at work on the basis of:

sex, race, ethnicity, colour, disability, age, marital status, religious or ethical belief, family status, sexual orientation, political opinion, employment status or involvement in union activities; or

an employee refusing to do work on the belief that it would be likely to cause serious bodily harm.

Harassment at work. Failure of the employer to take suitable steps to deal with a reported harassment would be sufficient grounds for a grievance claim.

If an employee does not raise a grievance within 90 days of becoming aware of it, then the employer is under no obligation to consider the issue. However, the courts may make exceptions especially if the employer had no agreement in place and no policies or means of ensuring that the employee was aware of the time limit. The grievance must be brought against the employer within 90 days of the employee becoming aware of the event or issue giving rise to the grievance.

26.4 Remuneration And Payment Issues

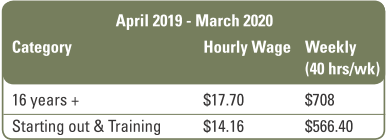

26.4.1 Minimum Wage

The minimum wage is set around March of each year. The following table summarises the minimum wage that an employer is required to pay employees before tax:

Check our website for updates.

A ‘Starting Out Wage’, at 80% of the adult wage, applies to:

• 16-17 year-olds in their first 6 months in a job;

• 18-19 year-olds entering the workforce after spending more than 6 months on a benefit; and

• 16 to 19 year-olds in a recognised industry training course involving at least 40 credits.

If an employee is on commission or paid by piece rate then the wage must be topped up to the minimum wage when it falls below this level. All commissions, bonuses and other remuneration count when checking to ensure that the minimum wage has been met.

The training wage applies to people doing recognised industry training involving at least 60 credits a year.

26.4.2 Registration

When you start employing it is important that you register as a new employer (Form IR 334). Upon registration the Department will send you PAYE deduction tables.

26.4.3 Deduction of PAYE

As an employer you have the responsibility to deduct PAYE or withholding tax from the wages and salaries paid to your employees. Failure to forward source deductions to the Department is the most serious offence in the Tax Administration Act and can result in a fine of up to $50,000 and 5 year’s imprisonment.

The due dates for these payments depend on whether you are classed as a small or large employer. Employers whose total PAYE and employer’s superannuation contribution tax (ESCT) exceed the annual threshold of $500,000, are “large” employers and must pay their PAYE deductions to the IRD twice a month. Due dates for payment of PAYE and ESCT to the IRD are as follows:

Payday filing for PAYE

From 1 April 2019 you are required to file your employment information on a payday basis. Instead of filing an Employer Monthly Schedule (IR348) every month, you must file an Employment Information Schedule online every payday. The process has been built into major payroll software programs, so that the required information is transferred electronically to the IRD when you pay your employees.

The change relates to the transfer of information only. The payment dates for PAYE and other payroll deductions remain unchanged.

26.4.4 Employee Reimbursement

Generally, all monies paid by an employer to an employee are treated as taxable monetary remuneration. However, an employee is generally not taxed on the reimbursement of actual expenses incurred on behalf of the employer.

Example

An employee uses her credit card to book a place at a conference that she will attend on behalf of the business. The reimbursement of this actual expenditure by the employer will be tax free in the hands of the employee.

Note: the employer should retain copies of invoices and record the reasons why the reimbursement was paid tax-free. Expenses may also be reimbursed by way of a reimbursing allowance. The allowance reimburses an average or expected amount of employee business expenditure. An allowance that is in excess of the expenditure incurred by the employee may however be taxable and subject to PAYE, so care is required and records should be kept to make sure it is not excessive.

26.4.5 Reimbursement of Motor Vehicle Expenditure

Where an employee owns a motor vehicle and uses the vehicle for work related purposes, a number of methods of tax-free reimbursement can be used.

Cost Method: Firstly, you may reimburse your employees for their actual expenditure incurred. The employee keeps a detailed record of all invoices related to motor vehicle running and keeps a logbook identifying business trips. The expenditure incurred is multiplied by the business use percentage, resulting in an actual reimbursement figure. In practice, this method is used infrequently due to extensive record keeping requirements. As running costs increase however, this may become more worthwhile.

Kilometer Rate Method: Alternatively, employers can reimburse for actual kilometres travelled, based on a detailed employee record, using IRD rates (see below) or rates published annually by the AA (www.aa.co.nz).

General Allowance: Finally, many employers prefer to pay a general allowance to employees for business related travel. The onus is on the employer to establish that the general allowance is reasonable. A suggested approach involves affected employees (or a representative employee for a group of employees) keeping a logbook for a three- month period. The business related kilometres over this period can be grossed up/annualised and the IRD rate applied to construct a defensible allowance.

Kilometre Rates Method (ITA DE 2) for Employee Reimbursement and Self-employed

If you are self-employed you may use a kilometre rate method instead of actual costs to claim for business use of your vehicle.

This method may also be used to reimburse employees for business use of their vehicles.

If you wish to use this method, you must make an irrevocable election to do so when you file your tax return for the year in which you acquire the vehicle or first use it for business purposes. If you fail to do so, the default method is the cost method. Once established, you may not switch between methods for that vehicle. A record must be kept of all travel undertaken in the vehicle.

The Commissioner plans to set rates annually after 31 March, in two tiers:

Tier1: The rate for the first 14,000 kilometres p.a. will be set to recover both the vehicle’s annual fixed costs and it’s variable per kilometre running costs;

Tier2: For kilometres above 14,000p.a., the rate will cover running costs only, as all annual fixed costs of vehicle ownership would have been recovered by Tier1.

There is no longer a 5,000 km limit restricting the use of these rates. Where you use the kilometre rate method, there will be no depreciation deduction or recovery income following the disposal of the vehicle.

Example

Self-employed Miles Pavis buys a new hybrid car for personal and business use. He elects to use the per km method to calculate his vehicle deductions in his tax return. Business use, based on his log book, is 55%. Miles drove 34,000 km over the year.

The kilometre rate method is also available to employers for reimbursing employees who use their vehicles for business purposes and close companies may use it as an alternative to paying FBT (See Chapter 19). Where a close company uses this method there is no separate interest deduction in respect of that vehicle

26.4.6 Extra Pay and Emoluments

An extra emolument is a lump sum payment, made in the context of an employment relationship that is not overtime. This includes bonuses, gratuities, profit shares, back pay, redundancy pay and retirement allowances. These are now more commonly referred to as “extra pay” and have PAYE withheld at the time they are paid to the employee.

26.4.7 Holiday Pay

Holiday pay is part of ordinary wages and salaries of an employee and as such, is subject to ordinary PAYE tax deductions. You may claim a deduction for holiday pay in (say) Year1, if paid to the employee within 63 days after Year1’s balance date, or you may now choose to take the deduction in the year in which it is paid.

26.4.8 Shareholder Employees (ITA s EA 4)

PAYE must be deducted from shareholder salaries if the salary or wage is paid regularly:

in intervals of one month or less; or

the regular payment makes up at least 2/3 of the total salary/wage received as an employee.

Otherwise PAYE need not be deducted. Many shareholder employees prefer to have PAYE deducted from their salary. This is a conservative approach that minimises the provisional tax burden and reduces the risk of use of money interest being charged on underpayments of provisional tax. Some choose to pay end-of-year lump sum payments without PAYE deducted. The lump sum is deductible to the business in any income year if paid during the year or within 63 days after year end. You may choose instead to take the deduction in the year it is paid.

26.4.9 Gifts, Tips or Gratuities

A monetary gift or tip to an employee, relating to the employment, is treated as gross income of the employee and is subject to PAYE. Such gifts or tips are deductible to the employer. Non-monetary gifts are subject to the FBT regime (See Chapter 19).

26.4.10 Inducement Payments

An inducement payment to encourage a person to enter employment or remain in that employment is subject to tax at source, i.e. PAYE.

26.4.11 Restrictive Covenants

A restrictive covenant or restraint of trade payment is subject to tax at source, i.e. PAYE. For example, a key employee receives $20,000 in exchange for them agreeing not to compete with the employer when the employment relationship ceases.

26.4.12 Damages and Compensation

Payments that are genuinely and entirely for compensation for humiliation, loss of dignity or injury to feelings, are not monetary remuneration. Consequently, there is no requirement to deduct PAYE from these payments. However, PAYE must be deducted from payments ordered by the Court to a former employee for loss of wages or allowances.

26.4.13 Tax Free Employee Allowances

When negotiating salary packages, there is an opportunity to generate tax savings by paying genuine tax-free reimbursements for meals, mileage or tools. If employees are expected to incur business related costs, it is more efficient to pay a tax-free reimbursement or tax-free allowance than pay an additional taxable salary amount.

Accommodation provided by an employer is tax-exempt for employees expected to work out of town for up to two years; or up to three years if working on capital projects; or five years on Canterbury earthquake recovery projects. For employees working at more than one workplace on an on- going basis the tax exemption has no upper time limit. These exemptions do not apply to salary trade-off arrangements, or arrangements to restart an exemption period.

Taxable accommodation benefits are generally valued at market rental value, less an adjustment for work use of the property. For an overseas posting, this is capped at a New Zealand equivalent. For example, if an employee would normally work in Hamilton, the value of any taxable overseas accommodation provided would be capped at the average or median rents in Hamilton for similar lodgings.

Meals: Where an employee is required to work away from their workplace, any meal is non-taxable to the employee. For business travel, this is limited to three months, including transfers to a new work location and long term secondments.

Clothing allowances will not be taxed for employees required to wear distinctive work clothing. This includes an allowance for plain clothes allowances for those who are provided with a uniform but are required not to wear that uniform for certain duties.

26.4.14 Other Matters

One of the few offences in the Tax Administration Act that could lead to imprisonment is failing to pay over amounts that have been deducted for PAYE. The Department treats such an offence very seriously and may also impose significant penalties.

Even where an employer has paid a gross wage or salary to a worker (i.e., no PAYE was deducted) the Department can chase the employer for the PAYE and will do so regardless of the fact that the worker holds the gross amount.

It is important to ensure that all records and obligations regarding employment are carefully complied with. This will require good record keeping.

Where a remuneration package includes non-monetary benefits, then the employer will be liable for Fringe Benefit Tax.

Student Loan Deductions: Along with PAYE, employers are also required to make deductions from the salaries or wages of employees with student loans owing, at a minimum rate of 12% for every dollar over the repayment threshold $19,760 p.a. or $380/wk for the 2019-20 income year). For example, if your employee earns $600 a week before tax, your deduction will be $26.40 [($600 - $380) x

0.12=$26.40)]. An employee must repay 12% on all income (before tax) earned from secondary jobs. The IRD has a PAYE/KiwiSaver deductions calculator to check how much your repayment deductions will be.

26.5 Kiwisaver Scheme

KiwiSaver is a voluntary, work-based savings scheme to help New Zealanders save for their retirement. Inland Revenue administers the scheme using its longstanding PAYE system.

Enrolment

You are eligible to join KiwiSaver if you are:

Normally resident in New Zealand or you are living overseas in the employment of the NZ State services; and

Entitled to remain in New Zealand indefinitely.

So, for example, a New Zealand citizen normally living in Australia is not entitled to join unless employed by the New Zealand Government. An Australian citizen normally living in New Zealand is entitled to join KiwiSaver because they are entitled to be here indefinitely.

You can join KiwiSaver either by automatic enrolment or by opting in.

New employees must be automatically enrolled into KiwiSaver when they start a new job and remain in the scheme for a minimum of 14 days. They may then choose to “opt out” and must advise the IRD of their decision within eight weeks (56 days) from the day they start their new job if they do not wish to participate in the scheme. Scheme enrolment is not automatic for workers under 18, or for existing employees. They will be able to join by opting in if they wish. Self employed people, beneficiaries and children are also able to join by opting in but need to make payments directly to Inland Revenue.

Employer Obligations

The KiwiSaver Act imposes obligations on employers that are New Zealand resident or carrying on business from a fixed establishment here, in respect of their employees who are eligible to join the scheme. The IRD will send you their employers guide (KS4) explaining your role and obligations when implementing KiwiSaver. In brief, employers are required to:

Enrol employees if they are eligible. Complete the KiwiSaver employee details (KS1) form to notify the IRD about a new employee being enrolled automatically in KiwiSaver or an existing employee who opts in.

Give the KiwiSaver employee information pack (KS3) to new employees who qualify for automatic enrolment, and existing employees who want to opt in.

Provide new employees with a written statement if you have an “employer-chosen scheme”, and give them that scheme’s investment statement. Note, you may (but do not have to) choose a KiwiSaver scheme for employees who don’t choose a scheme of their own. Employees may choose or change their schemes at any time but can only have one provider at any time. Those who do not specify a fund will be randomly allocated to a default provider.

Deduct employee contributions from their first and subsequent pays, and make compulsory employer contributions (see below).

Forward the KiwiSaver contributions to the IRD by the due date along with your PAYE payments.

For employees who decide to opt out or suspend their savings:

action their opt-out and savings suspensions requests, and

notify the IRD, and

refund any contributions deducted, if not yet passed on to the IRD.

stop or start deductions as advised by IRD

Order KiwiSaver employee information packs (KS3) from the IRD.

Contributions

The minimum contribution to the KiwiSaver scheme for participating employees is 3% of their gross wage. These are deducted from the wage at the time it is paid to the employee and held back to be paid over to the IRD along with PAYE.

Employers must also contribute at least 3% of the employee’s gross wage to the fund of each employee who is a KiwiSaver or complying fund member. The employer may also choose to contribute 4%, 6%, 8% or 10% instead of the 3% minimum. You may contribute more than the minimum if you wish. Through good faith bargaining, a salary package may be negotiated whereby compulsory employer contributions can be offset against the employee’s gross pay. However, if you have already agreed to a total remuneration package with your employee, the compulsory employer contributions must be paid on top of that package. Your employee’s take- home pay may not be reduced because you are making a compulsory contribution.

The compulsory contributions apply to employees who are:

aged 18 or over; and are

contributing themselves to the scheme via deductions from their salary or wages; and are

not a member of a defined benefit scheme.

Penalties apply for failure to make compulsory employer contributions and amounts unpaid will need to be backdated.

Employer’s Superannuation Contribution Tax (ESCT)

All employer contributions to KiwiSaver and any other super scheme are subject to ESCT. Employers’ cash contributions can be treated as part of the employee’s salary or wage and taxed under the PAYE rules if the employer and the employee agree. Otherwise you can choose an ESCT rate based on the employee’s “relevant income” for the previous year (1 April to 31 March):

If the employee did not work a full 12 months in the previous year or starts work during the year, the rate is based on estimated relevant income.

ESCT is deducted from the amount to be paid to the employees’ KiwiSaver accounts, rather than being an extra cost to employers.

Note: Any ESCT rate set for any employee must remain the same for a full tax year. This means that only one rate can be used for any employee in any tax year. The only time you can change the ESCT rate is at the beginning of a new tax year.

Savings Suspension

Previously known as a “contributions holiday”, savers can now apply to suspend their contributions for up to a year at a time. Contributions resume after twelve months unless the individual applies for a further savings suspension.

Government Subsidies

The government adds to the employee’s savings by contributing 50c for every $1 contributed by members, up to $521 a year, by way of a “tax credit”. These payments are made annually after the government financial year.

Shareholder Employees

Shareholder employees on a salary are able to receive all the benefits as an employee, and deduct the employer contribution as an expense.

Access to Savings

Savings are primarily for retirement and “locked in” (i.e. will not be accessible) until the age of eligibility for NZ Superannuation, currently 65, at which point you will receive a tax-free lump sum.

Early access is available in cases of:

financial hardship

permanent emigration

death (where the savings form part of the deceased’s estate), or

after a minimum of three years, to contribute toward a deposit on a first home. A member’s tax credits are included in the amount that may be withdrawn for this purpose.

All withdrawals from your KiwiSaver account are tax-free.

Self-Employed

If you are self-employed, you can also join KiwiSaver. You need to choose a provider and apply directly to them. They will apply to the IRD on your behalf for the tax credit to go into your fund. Pay at least $20 weekly ($87 monthly) to get the full benefit of the credit at a rate of 50c to the $1.

Family members

The unemployed and children can also join KiwiSaver in the same way as the self employed. The regular contribution of $20 weekly is voluntary, but if you don’t pay, there will be no tax credit.

The tax credit is not available to anyone under the age of 18. A child who joins under the age of 18 will be required to contribute once they start earning.

The earlier one starts contributing, the higher one’s savings in retirement.

Note that neither the returns nor the capital value of KiwiSaver funds are guaranteed by the government and there will be times when funds lose value due to fluctuations in investments.

www.sorted.org.nz has a calculator to estimate what your savings will be worth at your retirement. This is also available via the FBA website (www.businessadvisor.co.nz).

Choosing a fund

Several financial organisations have been appointed by the Government to be default scheme providers. These are:

AMP Services (NZ) Limited

ANZ New Zealand Investments Limited

ASB Group Investments Limited

BNZ Investment Services Limited

Fisher Funds Management Limited

Grosvenor Investment Management Limited

Kiwi Wealth Limited

Mercer (NZ) Limited

Westpac New Zealand Ltd.

They offer a range of funds that vary in risk and expected return and can be summarized as follows:

In the above table, the investments are ranked with the low risk / low return option first and increasing in expected level of long-term return with higher associated risk as you progress down the table. Again it is stressed that the government does not guarantee your KiwiSaver account.

Exempt Employers

If your business has an existing superannuation scheme that meets certain criteria, you can apply to the Government Actuary to be exempt from enrolling new employees automatically in KiwiSaver. You may have the option to convert the existing superannuation scheme to a KiwiSaver

scheme or complying superannuation fund, or establish a KiwiSaver scheme as part of the existing scheme or continue to operate independently of KiwiSaver.

The Government Actuary may revoke the exempt employer status if the alternative fund no longer complies and from that date, new employees must be automatically enrolled in KiwiSaver.

26.6 Contractors’ Schedular Payments

Payments made to self-employed contractors may be subject to a withholding tax which you deduct from the contractor’s bill to pay the IRD. These are known as schedular payments. If you pay a labour hire business who pays the worker, the labour hire business must pay the withholding tax to the IRD. Withholding tax rates are set out on the Tax rate notification for contractors form (IR330C) that is filled in by the contractor for each employer. Contractors may choose their own withholding rate, subject to specified minimums. Contractors not previously affected may opt into the schedular payment rules if the payer agrees. Schedular payments include the following classes of service with the withholding tax rate varying depending on the activity:

commissions paid to insurance agents and subagents or to salesmen

company directors’ fees

boards of trustees and examiner fees

agricultural, horticultural and forestry work

mail delivery, transport of school children, milk delivery, refuse removal, caretaking, security duties, and street or road cleaning

non-residential cleaning, gardening, vermin or weed destruction

supervising examinations

supply of labour on building projects

fishing operations

casual agricultural workers

jockeys, drivers and their apprentices

photographers, journalists, writers and artists

fees for persons exhibiting appliances or equivalent items

fees for modelling

entertainers including non-musical entertainers and apprentice jockeys

honorary payments

election officers remunerations

payments made to people selling greenstone, eels, whitebait, and sphagnum moss

contract payments to non-resident contractors, non- resident entertainers visiting New Zealand or non-resident professional sports people (some exemptions apply.

See 18.2.8 re: Non-Resident Contractors Tax (NRCT).

26.7 The 90-Day Trial Period

You can hire new employees on a trial period of up to 90 calendar days. This does not apply when rehiring someone who has previously worked for you.

From 6 May, 2019, 90-day trials are only available for businesses with fewer than 20 employees.

An employee who signs that agreement will not be able to later make a claim of unjustified dismissal, though a personal grievance may be raised on other grounds such as discrimination.

The employer must comply with other terms of the contract such as giving the required notice to dismiss before the end of the probation.

It must be clear that the employee has accepted this clause prior to starting work with the employer for the first time. It is therefore recommended that the agreement be signed on a date prior to the first day on which your employee starts work with you.

26.8 Holidays And Leave Entitlements

The Holidays Act 2003 provides for all employees being entitled to Statutory (Public) and Annual Holidays. There can be some little catches in getting this right during special circumstances.

26.8.1 Statutory Holidays

There are 11 public holidays each year in New Zealand. Employees who do not work on a public holiday when they would otherwise have worked are entitled to be paid as though they had worked their normal hours. The Act sets out an employer’s rights to require employees to work as provided for in their employment agreement or if they agree to do so. So what are your obligations as an employer?

You are required to pay employees statutory holidays provided that they fall on a day on which employees would ordinarily work, with the exception of the Christmas and New Year provisions. If Christmas Day, Boxing Day, New Year’s Day or 2 January falls on a Saturday or Sunday, the Act transfers the paid holiday to the beginning of the following week.

If an employee works on a Public Holiday then you are required to pay that employee at the rate of 1.5 times pay and you are also required to give the employee a paid day off in lieu of the public holiday worked. Entitlement to alternative holidays remains until taken, and must be paid out on termination. If an alternative holiday has not been taken in the 12 months after it became due, the Act allows the employee to exchange the holiday for a payment.

You cannot contract out of your requirement to provide 11 days holiday simply by providing for the payment of penal rates on statutory holidays.

26.8.2 Annual Holidays

Employees become entitled to a minimum of 4 weeks paid annual holiday at the end of each 12 months of continuous employment with any one employer. Some employers may at their discretion provide their employees with longer annual holidays.

Employees who finish working for their employer are entitled to payment at 8% of gross earnings if they leave within their first year or otherwise for the period of untaken leave to which they are entitled at the date of termination.

An employer may allow an employee to take an agreed portion of the employee’s Annual Holiday entitlement in advance. Employers must allow employees to take at least 2 weeks of their Annual Holidays in a continuous period, if the employees wish to do so.

Annual Holiday must be paid for before the holiday is taken unless the employer and employee agree that the employee is to be paid in the pay that relates to the period during which the holiday is taken.

Payment for the holiday is the greater of the employee’s ordinary weekly pay before the holiday or average weekly earning for the 12 months immediately before the end of the last pay period before the Annual Holiday. Employers may allow employees taking Annual Holidays to take Sick Leave if they fall sick during their Annual Holiday.

If the employer observes a customary closedown (e.g. maintenance shutdown in July) then an employee who is entitled to Annual Holiday at the commencement of the closedown period must, if required to do so by their employer, take Annual Holidays during the closedown period. This requirement should be documented in the Employment Agreement. If the employee is not entitled to leave to cover the shutdown period, the employer may pay the employee for leave accumulated to the start of the closedown at 8% of gross earnings. The employee’s anniversary date is then changed to the start of the closedown period. This should also be built into the agreement allowing nominated closedown dates to be set as this may vary from year to year. If the closedown period is roughly at the same time each year then the employee will become entitled to 4 weeks leave if employed continuously from one closedown period to the next. The employer is only entitled to one customary closedown period per year for any employee or group of employees.

Employers must allow employees taking Annual Holidays to take Bereavement Leave. If the Sick Leave or Bereavement Leave has been exhausted, employers may allow the employees to take the leave as Annual Holidays.

The Act requires employers and employees to deal with each other in good faith. The employer must inform the employee about his or her entitlement under the Act which includes:

Public Holiday provisions and all other holiday provisions

Employment agreements must reflect the requirements of the Holidays Act 2003

Ensuring that records, holiday policies and procedures reflect at least the minimum provisions of the Holidays Act 2003

26.8.3 Sick Leave

There is no entitlement until after 6 months service. The employee then becomes entitled to 5 days Sick Leave. A further 5 days Sick Leave accrues every 12 months on the anniversary of 6 month’s service.

Sick Leave can be paid in advance and can be deducted from any future entitlements. Unused Sick Leave may be accumulated up to a maximum of 20 days. Unused sick pay on termination is not paid out. If the employee has used all of the Sick Leave entitlement then it may be agreed with the employer to use Annual Leave entitlement. Sick Leave also includes leave for a sick spouse or dependent.

Note that employees don’t have to use sick leave for time off resulting from an accident in the work place.

26.8.4 Bereavement Leave

Employees are entitled to bereavement leave if they have:

completed 6 months’ current continuous employment with the employer; or

worked for the employer at least an average of 10 hours a week, and never less than 1 hour in any week or 40 hours in any month, over a 6 months’ period.

On each death of a close relative, the employee is entitled to up to 3 days’ paid leave. This includes the death of the employee’s spouse, child, parent, sibling, grandparent, grandchild or the spouse’s parent. The leave can be taken at any time and for any reason relating to the death. Where more than one close family member dies the employee is entitled to 3 days’ bereavement leave for each person who has died. The pay is equal to the amount they would have been paid on the days off, based on their normal hours.

Where bereavement relates to someone who is not a close relative as listed above, the employee may be entitled to 1 day paid leave at the discretion of the employer. The employer is required to take the facts into account including the closeness of the person who has died, the responsibilities of the employee relating to the death or funeral and cultural considerations.

There is no maximum or cumulative entitlement. The employee is entitled to leave for every bereavement.

26.8.5 Domestic Violence Victim Protection Act 2018

From 1 May 2019, victims of domestic violence are eligible for 10 days paid leave a year. Like sick leave, employees may take this leave as required. Employers must work with affected employees to help them deal with the effects of domestic violence.

26.8.6 Parental Leave and Employment Protection Act 1987

Parental leave is funded by the Government and costs the employer nothing (except replacement labour).

Duties of the employer

Employers must advise employees of their parental leave entitlements, grant parental leave to all eligible employees and assist with the application process.

Application Process

After receiving an application, an employer has up to 7 days to request further information, which the employee must provide within 14 days. The application must be granted or declined with reasons in writing within 21 days. The letter should set out the employee’s rights and obligations and indicate whether the job will be kept open or not. The employee should be reminded of the obligation to provide at least 21 days notice before returning to work or advising of the intention not to return to work at the end of the leave.

Keeping the job open

Jobs must always be kept open for parental leave of 4 weeks and less. For longer leave, the job also has to be kept open unless the employee is in a key position and the employer can prove that it is not practical to employ a temporary replacement. If this applies, the employee must be given preference for any similar roles that become available within six months from the time leave ends.

An employer may make a position redundant while the employee is on parental leave. The employer will need to follow a fair and consultative process and be able to justify the redundancy if this is challenged.

Types of leave

There are 4 types of leave:

Special Leave: Up to 10 days for a pregnant mother, before maternity leave begins

Maternity Leave: From 1 July, 2018, up to 22 weeks paid by the government (increasing to 26 weeks in July 2020). Can commence up to 6 weeks before due birth date or taking a child up to 6 years of age into care for adoption.

Partner’s/Paternity Leave: 1 week if 6 month’s work with the current employer; or 2 weeks if 12 months service (hours test applies - see below); or up to 14 weeks if mother’s leave is transferred to the partner.

Extended Leave: Up to 52 weeks, less other parental leave taken, unpaid and dependent on hours test (see below).

All leave must be taken in the first year after the birth or adoption.

A parent who accumulates more than 52 hours of work during the leave is deemed to have returned to work and loses entitlement to further paid leave.

Eligibility for parental leave and hours test

Special leave, maternity leave, and partner’s/paternity leave, may be available to both male and female employees who have worked for the same employer for at least six months continuously prior to the expected date of birth (or date of taking a child into care for adoption). To qualify, they need to have worked at least 10 hours in every week or 40 hours per month. Since 1 April 2016, parental leave applies to more workers, including those who have recently changed jobs, seasonal and casual workers, and workers with more than one employer, primary carers, home-for-life parents and others with similar permanent care arrangements.

Extended leave is available to both males and females who have worked for the same employer as above for at least 12 months. The partner’s/paternity leave entitlement also increased from 1 week to 2.

26.9 Health And Safety

The Health and Safety at Work Act 2015 (HSWA) places primary responsibility on the person conducting the business or undertaking (PCBU) to take “reasonably practicable” steps to ensure the health and safety of workers and others in the workplace.

Meaning of reasonably practicable

In the Act, reasonably practicable in relation to a duty of a PCBU means that which is, or was, at a particular time, reasonably able to be done in relation to ensuring health and safety, taking into account and weighing up all relevant matters, including:

(a) the likelihood of the hazard or risk occurring; and

(b) the degree of harm that might result; and

(c) what the person concerned knows, or ought reasonably to know, about the hazard or risk and ways of eliminating or minimising the risk; and

(d) the availability and suitability of ways to eliminate or minimise the risk; and

(e) after assessing the above, the cost associated with available ways of eliminating or minimising the risk, including whether the cost is grossly disproportionate to the risk.

Officers, including directors must exercise due diligence to ensure the PCBU meets its health & safety obligations and workers and others in the workplace have a responsibility to keep themselves and each other safe.

The Act is supported by regulations. Writing and implementing a Health and Safety Manual for your workplace is strongly advised. This does not need to be a huge document but should set out the policy and advise staff of the legal requirements and business expectations.

Involve your staff in decisions that affect them. Familiarise yourself with your responsibilities under the new regime and ensure that adequate training is provided at your work. You cannot contract out of your duties and consequences of failing in this area are severe.

26.9.1 Compliance

In order to comply with the Act you need to fulfil the following:

Identification and assessment of all hazards at your work place. Where hazards have been identified ensure that adequate precautions are in place.

Employees should contribute to hazard identification. If an employee approaches you regarding a potential hazard we suggest you take action immediately.

Ensure that all options for the safety of employees and persons other than employees have been considered. Do your employees understand these procedures? Do they understand the emergency procedures?

Adequate training and supervision of employees will be necessary to avoid an accident or injury.

Are there procedures in place in the event that an accident occurs? Maintain an Accident/ Incident register, investigate accidents and advise WorkSafe NZ of any that cause serious harm.

Have you considered how to manage your safety policy to cover the event of visitors or contractors on your premises?

Depending on the nature of your work, special advice may be necessary. Consultants in Health and Safety are readily available and the Department of Labour is extremely helpful.

26.9.2 Rest and Meal Breaks

From 6 May, 2019, all employers must provide employees with at least the following paid rest breaks and unpaid meal breaks:

one paid 10-minute rest break when they work for 2 to 4 hours;

one paid 10-minute rest break and one unpaid 30-minute meal break when they work from 4 to 6 hours; and

two paid 10-minute rest breaks and one unpaid 30-minute meal break when they work for 6 to 8 hours.

If the employee works continuously for longer than 8 hours, these requirements automatically extend to cover the additional hours on the same basis.

The timing of breaks is by agreement. If agreement can’t be reached, the breaks must be spread evenly throughout the work period if reasonable and practical. Where an employee is required to take a rest break under another Act, then that overrides the general rules above.

26.9.3 Infant Feeding

All employers must provide facilities and unpaid breaks for employees who wish to breastfeed their infants during working hours. This includes expressing breast milk.

In short, reasonable and practical arrangements must be made. For example: The employee must be provided with an appropriate private space and access to a fridge.

The breaks are to be unpaid and provided over and above normal rest breaks unless otherwise agreed.

26.9.4 Other Health and Safety Issues

WorkSafe NZ is the regulator under the HSWA. They have produced a guide on the new Act.

Maximum penalties under the Act are for reckless conduct in respect of duty that exposes an individual to a risk of serious injury, serious illness or death. These penalties are:

a. For a business: $3 million fine

b. For an officer: Five years in prison, or $600,000 fine, or both

c. For others: Five years in prison, or $300,000 fine, or both

Note that you cannot insure against these fines.

Stress and fatigue are a workplace hazard. With personal grievance claims related to workplace stress increasing at a significant rate, this could have serious consequences for many employers whose employees are working extended hours or are having outside personal problems that are causing them undue stress.

What employers need to do is take proactive steps in monitoring employee mental health and preventing stress in the workplace. This should include training on time and stress management, doing hazard audits on fatigue and stress and providing access to counselling services.

One would also expect to see more restrictions set on secondary employment and a limit to overtime or extended hours worked.

26.10 Drug Testing

Drug testing in the work place can serve to avoid potential compromise of safety to other employees where the use of drugs may create a potential significant hazard. In this context drug testing includes the testing for alcohol and other substances that may affect work place performance.

If the employer wishes to consider drug testing in the work place it should be included in the employment contract. An employer’s drug and alcohol testing should be adopted only under the following circumstances:

Test when there is an identifiable problem in place – this adds economic and legal weight to the decision to test

Minimise the extent to which employees may be humiliated

Employees should consent to the testing prior to it taking place (hence it would be useful if drug testing was covered in the Employment Agreement)

Employees should be aware of the drug testing policy and the consequences of failing any tests

Controls need to be in place to preserve the confidentiality of drug test results

26.11 Smoke Free Environments Act 1990

Under the requirements of the Act, all workplaces must have a policy on smoking, and must review that policy annually.

it is illegal for any person (including parents and other family members) to give cigarettes to under-18s in a public place.

there is a complete ban on smoking in indoor workplaces and in indoor areas of pubs, restaurants and other hospitality venues

there is a complete ban on smoking in schools and early childhood centres, both indoors and outdoors

cigarette vending machines can be operated only by staff members of the premises

In most cases it’s illegal to advertise cigarettes and other tobacco products

26.12 Volunteers Employment Protection Act

This Act protects the employment, under certain circumstances, of employees who volunteer for full time training of up to 3 months in the Armed Forces, or part time training of no more than 3 weeks in a year. The Act requires the granting of unpaid leave for this purpose. Where the Act applies, the employee’s position must be kept open, and for certain purposes, including rights and benefits that are conditional on unbroken service, the employment is deemed to be continuous.