Chapter 23 – Tax Administration

23.1 Overview

Under the Tax Administration Act 1994, all taxpayers are required to:

Correctly determine the amount of tax payable

Deduct or withhold the correct amount of tax from payments or receipts

Pay tax on time

Keep all necessary information and maintain all necessary accounts

or balances

Co-operate with the Commissioner

Comply with other specific tax obligations

Compliance obligations imposed on business and commercial activities are considerable. To list just a few, these compliance obligations include requirements to:

obtain an IRD number

register for GST if turnover exceeds the threshold (see Chapter 20)

file a regular GST return if registered

file an annual income tax return

pay provisional tax

deduct resident withholding tax on interest paid to other parties (excluding banks)

deduct PAYE and withholding tax from payments made to employees and contractors

deduct ACC payments

keep business records (including log books, expense invoices, and wage records)

calculate and pay fringe benefit taxes

maintain imputation credit accounts for companies

Unless these matters are handled by a bookkeeper or dealt with efficiently, a considerable amount of your otherwise productive business time will be expended in complying with your basic tax obligations.

23.2.1 Shortfall Penalties – Warning

23.2.2 Correction of Minor Errors (TAA s 113A)

23.3.1 Applying for an IRD Number

23.3.2 Balance Dates

23.3.3 Income Tax Return Types

23.3.4 Filing Requirements for Individual Taxpayers

23.3.5 Retention of Records

23.3.6 Personal Taxpayers and Attribution Rules

23.3.7 Tax Credits (Formerly Rebates) (ITA Part L)

23.3.7.1 Independent Earner Tax Credit (s LC 13)

23.3.7.2 Donations to Charitable Bodies (ITA Subpart LD)

23.3.7.3 Working for Families Tax Credits (ITA Subparts MC, MD & ME, s LB4)

23.3.8 Children

23.3.9 Gift Duty

23.3.10 Transfers of Overpaid Tax

23.2 Application

23.2.1 Shortfall Penalties – Warning

The IRD are now scrutinising errors on tax returns very carefully to ascertain whether any shortfall penalties should be imposed on tax shortfalls arising from lack of reasonable care, unacceptable interpretation, gross carelessness and evasion.

If in doubt about any tax matter, contact your tax advisor or the IRD. Under the IRD’s draft guidelines, you are considered to have taken reasonable care if you consult your tax advisor or IRD, present the full facts to them, and follow their advice.

23.2.2 Correction of Minor Errors (TAA s 113A)

Minor errors in a return are up to $1,000 in tax or, subject to the IRD’s discretion, errors found from 18 March 2019 that are equal to or less than the lower of $10,000 or 2% of the taxpayer’s gross income. These may be corrected in the next subsequent return after discovering the error. This applies to income tax, FBT, and GST returns. For larger errors, amended returns must be filed.

23.3 Practical Issues

23.3.1 Applying for an IRD Number

Applications for an IRD number can be made for:

Individuals on the IR595 form – this includes applications for children under 16 years old; and

Non-individuals including companies on the IR596.

Individuals

Individuals applying for an IRD number must front up in person to an AA Driver Licensing Agent, Postshop or selected New Zealand Post retail outlet with a completed IR595 form (that may be downloaded from the IRD website) and ID documentation as described in the IR595 form that sets out all details you need to know to complete the process.

Non-individuals

The Department will require the following proof of identification before processing each application:

Companies: Certificate of Incorporation

Trusts: Trust Deed

Incorporated Societies: Certificate of Incorporation

When a company is incorporated online through the Companies Office website, www.business.govt.nz/ companies, there is an option to apply automatically for an IRD number there and then.

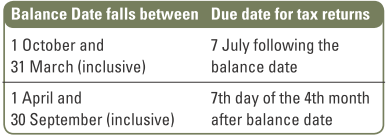

23.3.2 Balance Dates

Having received your IRD number, you will be required to file annual income tax returns. The standard income tax year runs from 1 April to 31 March. However it is possible to have an alternative balance date where an application is made to the Department.

The following activities will generally be granted the following non-standard balance dates.

A non-standard balance date may also be granted to:

Subsidiary companies, which may obtain the balance date of a parent company

Administrators of estates, which may obtain the balance date of the deceased taxpayer

Shareholders/employees, who may obtain the balance date of the company in which they are major shareholders

23.3.3 Income Tax Return Types

Different income tax return types are applicable for different classes of income taxpayers:

IR3: natural persons who are provisional taxpayers. (See Chapter 17)

IR4: companies other than LTCs

IR6: trusts and estates

IR7: partnerships and Look-Through Companies

IR8: Maori authorities

IR9: clubs and societies

Tax returns must be filed by due date. These depend on your balance date as follows:

If a tax agent completes your return there may be an extension of time for filing it. Check with your agent. The extension could be up until 31 March in the year following the income year for which the return applies. That is, the return may be able to be filed up to 12 months after year end under the extension of time arrangement.

23.3.4 Filing Requirements for Individual Taxpayers

Certain taxpayers are excused from having to file an income tax return. These include natural persons who:

Have all of their income taxed at source (i.e. income from employment, which is subject to PAYE, interest and dividends, which are subject to RWT). Non-taxable income such as certain distributions from Maori Authorities would also qualify as no tax is payable; and

Derive $200 or less of gross income that has had tax deducted incorrectly; and

Together with their spouses, did not earn over the threshold (currently $42,700) and receive Working for Families Tax Credits from Work and Income;

Did not use a special tax code or the wrong code

Did not have a student loan interim assessment – (where not enough has been deducted from your salary); and

Did not pay tax as an IR 56 taxpayer (home help, nanny, gardener, embassy staff, overseas company representative or “Deep Freeze” personnel in Antarctica.

In 2019 the IRD changed the individual tax assessment regime. Personal tax summaries (PTS) will no longer be issued. Instead, they will send you an income tax assessment to finalise your end-of-year tax information if your only income is from:

employment (such as salary and wages)

schedular payments (including ACC attendant care)

income tested benefits • interest or dividends

taxable Māori authority distributions

benefits under an employee share scheme

New Zealand superannuation (NZ Super)

student allowance

Accident Compensation Corporation (ACC)

Superannuitants will be advised how much they have received and how much tax was deducted in the year.

Taxpayers who do not meet these criteria must complete an individual tax return (IR3). They must request a Summary of Earnings (SOE) if the IRD has not issued one. This shows all income from employment, benefits and withholding payments for the year. It also shows the tax deducted at source and includes a calculation of ACC earners’ levy on employment income.

The SOE helps you to complete your IR3 as you are able to transfer the relevant figures from the one to the other before adding additional income that did not have tax deducted at source such as rent and self-employment income. If you disagree with the Summary of Earnings then you must notify the IRD with the correct information by the later of 7 February of the next income year or 30 days after the date the SOE is issued.

PAYE is discussed more in Chapter 26: Employment Responsibilities

23.3.5 Retention of Records

Any taxpayer in business is required to retain their business records for a period of seven years after the end of the income year to which they relate. These records include bank statements, invoices, till receipts and other sales records.

Recipients of investment income are also required to keep a record of this income for a period of seven years after the end of the income year to which it relates.

23.3.6 Personal Taxpayers and Attribution Rules

The income of individuals is taxed on a sliding scale with marginal tax rates increasing with the level of personal income. The individual tax rates are summarised in 2.2.1.

With the top marginal tax rate higher than the flat company rate, individuals providing personal services may have been tempted to divert income to interposed entities to be taxed at lower rates. For example, instead of charging clients directly, a consultant could operate through a company and benefit from the lower company tax rate. To prevent individuals from doing this, the attributed personal services income rules were introduced. These rules attribute personal services income of any interposed entity to the individual who provides the services. These rules apply where all of the following conditions are met:

the interposed entity and the individual service provider are associated;

80% or more of the interposed entity’s service income is derived from one customer (or a group of associated customers);

80% or more of the interposed entity’s service income relates to services provided by one employee (or relatives);

the employee’s net income in the year, including the attributed income, exceeds the personal services income threshold; and

Substantial business assets do not form a necessary part of the process of deriving the interposed entity’s income from services

If you are in the business of providing personal services through an interposed entity and have most income from one source, you should consult your tax advisor to determine whether the rules apply to you!

23.3.7 Tax Credits (Formerly Rebates) (ITA Part L)

A tax credit is a reduction in the amount of tax you need to pay. Taxpayers have 8 years in which to file their tax credit claims (IR526) such as donations to charities.

Available credits are summarised below:

23.3.7.1 Independent Earner Tax Credit (s LC 13)

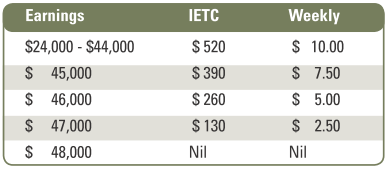

Eligible individuals earning between $24,000 and $44,000 inclusive may receive an independent earner’s tax credit (IETC) of $520 p.a. or $10 per week. The annual IETC entitlement decreases by 13 cents for every additional dollar earned above $44,000, up to $48,000. This is demonstrated in the example below.

Eligibility rules include:

New Zealand tax residency;

Neither the taxpayer nor a partner is entitled to working for families tax credits, nor receiving an overseas equivalent;

Not receiving a NZ income-tested benefit; and

Not receiving New Zealand Superannuation, Veteran’s Pension or an overseas equivalent.

To receive the IETC weekly as part of their pay, employees will need to fill out a new IR330 form selecting one of the two tax codes from above and forward to payroll. The new tax codes are:

ME for non-student loan borrowers who qualify, and

ME SL for student loan borrowers who qualify.

23.3.7.2 Donations to Charitable Bodies (ITA Subpart LD)

One third of all charitable donations are refunded by way of tax credit up to the total taxable income of an individual. A company may deduct donations up to its net income.

23.3.7.3 Working for Families Tax Credits (ITA Subparts MC, MD & ME, s LB4)

Working for Families Tax Credits are entitlements for families with dependent children aged 18 or younger. There are four different types of payments (tax credits). These are:

Family tax credit.

In-work tax credit

Minimum family tax credit

Parental tax credit

You may qualify for one or more of these credits. The entitlement varies depending on family income, number and age of dependent children and family work circumstances.

The IRD has online calculators and worksheets to help you work out your entitlement if any. Go to www.ird.govt.nz, click on “Work it Out” in the right column and choose Working for Families Tax Credits. Select the onscreen calculator for the applicable income year and complete the questions online. This is totally anonymous, quick and simple. You may be pleasantly surprised to discover your entitlement and may then apply online to receive it.

23.3.8 Children

The tax credit for children has been replaced by a limited tax exemption. School children do not need to declare untaxed income of less than $2,340. This exemption does not apply to salary or wages, or other income on which tax has already been paid.

23.3.9 Gift Duty

Gift Duty has been abolished. Taxpayers wishing to restructure their affairs to take advantage of this are advised to seek professional assistance, as this is a smart move for some and a costly mistake for others, depending on your circumstances.

23.3.10 Transfers of Overpaid Tax

The IRD now allows common transfers of overpaid tax to be made. This allows you to improve cash flow and cut use of money interest charges and other penalties.

23.3.10.1 Transfers to Associated Taxpayer

Transfers to associated taxpayers can occur for:

Overpaid income tax

GST refunds

Tax credits

Use of Money Interest

Taxpayers may transfer overpaid tax to another period or different type of tax. For example, transfer of GST refunds to cover a provisional tax liability.

There are rules governing the timing of transfers so that these are not made prematurely but rather as early as possible to help reduce the exposure to use of money interest and late payment penalties.

23.4 Practical Hints

23.4.1 Tax Filing and Wall Planner

The tax compliance requirements imposed on small businesses are considerable. If you are to maintain your focus on business and commercial activities, it is essential that your tax matters are dealt with efficiently. If you are to achieve this efficiency you can also save on considerable penalties for late payment of taxes.