Chapter 21 – Accident Compensation

21.1 Overview

Accidents and injuries in New Zealand are covered by a publicly funded insurance scheme administered by the Accident Compensation Corporation (ACC).

Businesses pay levies to cover work- related injuries and deduct premiums for non work-related incidents from employee salaries through the PAYE system. Self employed individuals pay levies to cover their own injuries, whether work-related or not. Vehicle accidents are funded through the vehicle registration system.

The residual claims levy for funding outstanding claims relating to accidents prior to 1 July 1999 has finally been removed, with claims having been settled.

The annual levy is effective each year from:

1 April for the Work and Earners’ Accounts; and

1 July for the Motor Vehicle Account.

All businesses pay levies to ACC to cover the cost of injuries. Whether you are self-employed or a business employing others, you’ll pay:

The Work Levy to cover work-related injuries;

Working Safer Levy which is collected on behalf of the Ministry of Business, Innovation and Employment (MBIE) to fund the activities of WorkSafe NZ.

Non work-related injuries are funded through the Earner’s Levy by employees and people who are self-employed.

Employee payments are made via deductions from their income with PAYE and are paid over to the IRD who collects the amounts on behalf of the Accident Compensation Corporation (ACC). The amounts are built into the PAYE tables.

The IRD shares necessary information with ACC who invoices employers and the self-employed for other amounts owing.

21.1.1 Earner Levy

The Earner’s Levy combined rate per $100 liable earnings for 2019-2020 is $1.39 including GST (unchanged from 2018-2019), subject to maximum liable earnings (See 21.2.1). For employees, the premium and levy is deducted by the employer with PAYE deductions and paid to Inland Revenue on the same due dates for PAYE.

Self-employed individuals are invoiced directly by ACC based on information supplied by the IRD.

21.1.2 Employers - Workplace Cover

ACC is the sole provider of workplace accident insurance in New Zealand.

All employers are required to pay employer premiums to cover workplace accidents. The employer premium payable depends on each employer’s industrial classification, which may vary from year to year (see 21.3.1). ACC bills employers for levies to cover the premiums.

21.1.3 Self-employed

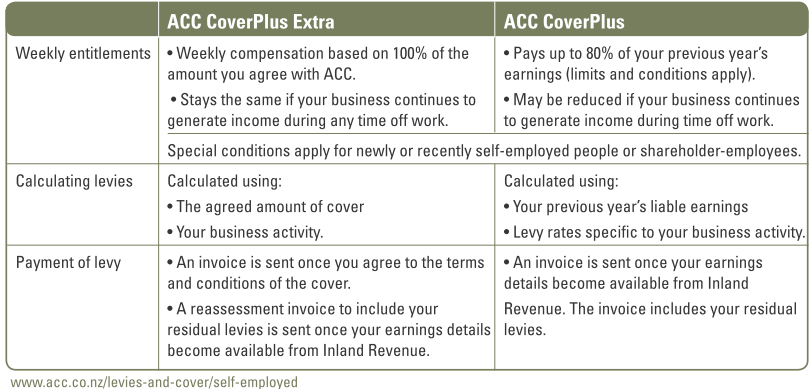

People who are self-employed also pay a levy to cover work related accidents. ACC offers two alternative policies invoiced in August each year when the information becomes available from the IRD based on the individual’s IR3 return. This determines both the levy and levels of entitlement.

ACC CoverPlus is the standard level of cover that entitles you to compensation based on 80% of your past year’s earnings from self-employment. You may also be eligible to take out extra cover in a separate policy known as ACC CoverPlus Extra that will entitle you to 100% of an agreed compensation if you are unable to work. The table below is provided by ACC and summarises the difference between the two options below.

21.1.4 Working Safer Levy

This levy is payable by employers and self-employed people and is collected on behalf of the Ministry of Business. Innovation and Employment to fund the activities of Work Safe New Zealand. It is included in the annual ACC invoice sent to employers and the self-employed.

The role of WorkSafe is to promote safer workplaces and investigate incidents where serious harm occurs or is likely to occur. This levy is currently charged at a flat rate of 8c (incl GST) per $100 of liable earnings.

21.2 Application

21.2.1 Maximum & Minimum Levies

The work place levy and the self-employed work account premium are subject to minimum and maximum levels of liable earnings, which can vary from year to year.

For 2019-20, the proposed maximum liable earnings fo:

• Employees and shareholder employees: $128,470 (prev $126,286) for the work place levy; and for

• Self-employed: $128,470 ($124,053)

Where a self-employed person works at least 30 hours per week on average and earns less than the prescribed minimum income level, the levies are based on the minimum prescribed liable earnings of $ 36,816 ($32,760). The figures are summarised in a table in the Appendix on Page 116 and come from ACC’s consultation document.

Liable earnings generally includes all income derived from personal effort. Earnings not liable for premiums include:

Interest and dividends or estate and trust income

Rental income, lease and bailment income, or royalties

Income-tested benefits, pensions, New Zealand superannuation or living alone payment

Student allowances

Retiring allowances and redundancy payments

Jury and witness fees

Non-taxable allowances or exempt income

21.2.2 Deductions

ACC levies and premiums are generally deductible in the year in which they become due and payable by the taxpayer. The GST component on the ACC levies and premiums can be claimed as a GST input tax credit.

21.3 Practical Hints

21.3.1 Classification Units

The amount your business pays to cover injuries depends on:

your business description — ACC assigns a classification unit (CU) based on your risk profile

how much you pay your employees

your claims history — the number of work-related injury claims your business has made.

CU is the classification unit description. This represents a group of businesses with a similar risk of workplace injury. Each CU has its own ACC levy rate, used to calculate levies for workplace injury cover. Each CU description has its own unique CU code.

Businesses with more than one distinct business activity may qualify for two or more CU rates. Contact the ACC Business Service Centre on 0800 222 776 if this applies to you, or if you have changed your business activity through the year.

Classifications may be obtained from www.businessdescription.co.nz where you can search online, download a booklet in pdf format or order a hard copy to be sent to you.

Example

Bob the Builder builds and renovates residential homes. To find his classification unit, Bob can download the current ACC Levy Guidebook from www.acc.co.nz. Instead, he goes to the website: www.businessdescription.co.nz.

He enters “Builder” in the search box on the right. He scrolls through the results and chooses:

House construction, alteration, renovation or general repair

This is has a Business Industry Code (BIC) of E301130. This is the code he provides to the IRD in his tax return to ensure that the correct levies are charged by ACC.

He clicks on “more” and is offered a number of other possible codes to consider, that may reflect the nature of his work more accurately, but decides that the above BIC best describes what he does.

He scrolls down and finds “Classification Unit (CU): 41110 - House construction This is used by ACC to calculate yourlevies.”

If more than one CU is applicable and you are:

a self-employed individual: The CU with the highest levy rate must be used

a business: The CU with the highest levy rate must be used, unless you are eligible to be assigned multiple CUs.

See 21.3.2 for using this code to estimate your levies. ACC invoices are sent based on the relevant earnings data provided by Inland Revenue from returns filed. There is no requirement to file a separate form.

Employers are required to pay the levy by 31 May each year.

21.3.2 Estimating your levies

The easiest way to estimate your levies is to enter them in the ACC website calculator. Refer to the Builder example in 21.1.2 to obtain your BIC and CU.

Step 1: Determine your Classification Unit (CU) from the website www.businessdescription.co.nz (See 21.3.1).

Step 2: Go to the following ACC website: www.levycalculators.acc.co.nz

Choose the appropriate form to fill in and follow the prompts. Tick the LCI box to adjust for the labour cost index.

21.3.3 Discounts Available

From 1 April, 2017, ACC’s Workplace Safety Discount (WSD) for small businesses and self-employed people has been discontinued.

If you’re on the WSD programme, your discount will continue until its expiry date. There is, however, a no- claims discount for employers and self-employed people who have paid under $10,000 in levies in each of the three previous years. About 35% of New Zealand businesses qualify for the No-Claims Discount Programme.

Those with a very good claims experience can receive a 10% discount on their Work levies, while those with a poor claims experience could receive a 10% loading. There also remains an experience rating incentive for larger businesses that have paid levies of over $10,000 in at least one of the preceding three years.

They may receive a discount or loading of up to 50% depending on their safety record based on injury rates and rehabilitation/return-to-work history.