Chapter 11 - Business Structures

11.1 - Overview

Your business structure can have a huge impact on taxation and the legal framework under which your business operates. Here, we compare the different business structures available to you. These are discussed in greater depth in following chapters.

11.3.1 - Advantages of a Sole Trader Structure

11.3.2 - Disadvantages of a Sole Trader Structure

11.3.3 - Changing Structure

11.3.4 - Recommendations

11.4.1 - Advantages of Partnership Structure

11.4.2 - Disadvantages of a Partnership Structure

11.4.3 - Recommendation

11.5 - Limited Partnerships Structure

11.5.1 - Advantages of a Limited Partnership

11.5.2 - Disadvantages of a Limited Partnership

11.5.3 - Recommendation

11.6.1 - Advantages of a Company Structure

11.6.2 - Disadvantages of a Company Structure

11.6.3 - Qualifying Companies

11.6.4 - Recommendation

11.7.1 - Advantages of a Trust Structure

11.7.2 - Disadvantages of a Trust Structure

11.7.3 - Recommendation

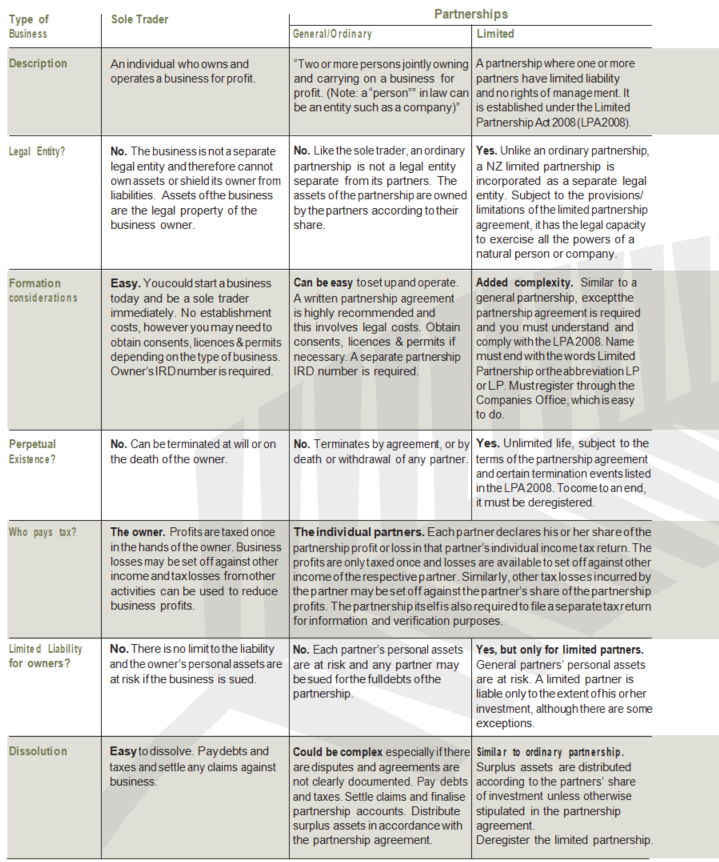

11.2 - Available Structures

Choices are available when considering how your business or commercial activity should be set up. You may choose to operate as a:

A) Sole Trader

B) Partnership

C) Limited Partnership

D) Company

E) Look-Through Company (LTC)

F) Trust

Your choice of structure will be influenced by the advantages and disadvantages of each structure (See summary).

Here, we consider the options and provide some recommendations. Chapter 12 deals with companies in more depth and Chapter 13 looks at partnerships, trusts and also covers some mixed structures.

As will be seen, it is both possible and advisable to separate your business from your personal assets and this may involve taking advantage of the benefits of more than one structure.

11.3 - Sole Trader

Running a business as a sole trader is generally most appropriate for small businesses which do not employ staff and which do not have significant commercial risks.

This structure starts to become less tax efficient at income levels around $44,000. (See 2.3.3 and 23.3.7.1).

11.3.1 - Advantages of a Sole Trader Structure

Uncomplicated: A sole trader structure is simple and involves minimal set up costs and administrative requirements. You would require an IRD number, GST registration perhaps, a file of business expenses and a bank account. You could operate with a small business accounting package or possibly even an invoice book (for your billings) and a cashbook. There is no need for separate stationery such as letterheads. Each year, you would file an IR3 tax return. Your accountant can provide details on these requirements.

Ownership: Effectively you are the business. You have sole responsibility and can make all decisions, without being accountable to anyone but yourself (and your customers, of course).

Tax losses: You will be able to access tax losses arising from your trading activities to set off against other income. Similarly, tax losses from other activities can be used to reduce the taxable income of your business. Unutilised tax losses may be carried to the subsequent income year.

Tax Rates: A sole trader is taxed at individual tax rates. At lower levels of income, the marginal tax rate of a sole trader is considerably lower than the flat rates of a company or trust as shown in Chapter 2.

Example

Ida Plut’s business earns net income of $42,000. She is in a two income family and decides to leave the profit in her business to grow it. The tax payable will be very different depending on the structure as shown in the table below:

Up to $48,000, the marginal tax rate for individuals is considerably less than the company tax rate subject to any IETC claw back (See 2.3.3, 23.3.7.1).

The current top marginal tax rate for individuals is equal to the trustee rate of 33%. So, all other things being equal, individuals do not pay higher tax than a trust at any income level.

11.3.2 - Disadvantages of a Sole Trader Structure

Liability is unlimited: A sole trader does not have the advantage of limited liability that is available to owners of companies. If a sole trader’s business fails, the sole trader will be personally liable for all debts, (including salaries, wages, holiday pay, all outstanding purchases of trading stock, all taxes and GST payable, and all interest and principal amounts on borrowings outstanding). Also, the sole trader’s other assets (home, cars etc) may be at risk.

Image: This structure projects the image of a small operator. As your business grows in size, a more sophisticated business or commercial structure may be required.

Tax: At higher levels of income, it is not tax efficient to operate as a sole trader.

11.3.3 - Changing Structure

A move from the sole trader structure to a company or trust will create a disposal of depreciable assets. Assets are generally deemed to be sold at market value between related parties. If the market value exceeds the tax book value, the disposal will create income in the form of taxable depreciation recovery for the sole trader.

11.3.4 - Recommendations

When you are first starting out in business and there is minimal risk of being sued, it is not a bad idea to prove the feasibility under a sole trader structure. If you plan to stay small and your risks remain low, there may be no compelling reason to change structure.

If you are thinking of growing, the sooner you switch to another structure (probably a company) the better, to avoid the tax consequences referred to above.

As a sole trader, it is highly recommended that you protect your assets from creditors and others, by putting your family home, business premises and other large assets into separate structures such as trusts or companies.

11.4 - Partnership Structure

A partnership is two or more persons, or companies, carrying on a business or commercial activity with a common view to making a profit. In practical terms, a partnership is normally evidenced by a partnership deed and the partnership will normally have a partnership bank account. This form of structure has been common for family businesses.

Because the partnership is not a separate legal entity, the partnership does not pay tax in its own name. It must, however, file a partnership income tax return (IR7). The profits or losses of the partnership are attributable to the individual partners. It is the partners who are responsible for the tax obligations on their partnership income.

11.4.1 - Advantages of Partnership Structure

The documentation required to establish a partnership can be straightforward. In practice, you would be well advised to obtain professional advice if you are thinking of running a business as a partnership

All profits of the partnership are attributable to the individual partners. This means that partners are taxed at the individual marginal tax rates - on their portion of partnership income, giving families a legal way to split income and reduce taxes

All losses of the partnership can be passed on to the individual partners. These losses can be set off against other sources of income to reduce the liability

Ability to pay working partners PAYE deducted wages and so have a portion of tax-paid income from the business.

11.4.2 - Disadvantages of a Partnership Structure

All partners to the partnership are jointly and severally liable for all liabilities of the partnership. This means that any one or more of the partners may be sued for all of the partnership debts.

A partnership (like a sole trader) does not offer the protection of limited liability. As a result, your personal assets can be called upon to satisfy debts incurred by the partnership.

For tax, partners are treated as carrying out their share of the partnership business separately. They also own their respective share of the underlying assets and liabilities. Separate tax returns need to be filed.

The Commissioner has discretion to reallocate partnership income or losses between relatives if in his opinion the allocation made is not reasonable (ITA GB23).

Changing partners could have undesired consequences (See 13.1.3.4)

11.4.3 - Recommendation

A partnership can be a suitable business structure if there are two or more participants involved and potential liabilities are not a major issue. If you operate through a partnership structure, you should at least consider putting your home and investments in an asset protection trust or company.

Partnership structures are discussed in further detail in Chapter 13 “Partnerships and Trusts”.

11.5 - Limited Partnerships Structure

The Limited Partnerships Act (LPA) came into force to make it easier for New Zealand businesses to attract investment capital and to compete internationally. Limited partnerships involve:

“General partners” who are jointly and severally liable with the partnership for its debts (LPA s 26-28). At least one general partner must be resident in New Zealand or Australia;

“Limited partners” who are only liable to the extent of their capital contribution to the partnership (LPA s 31);

Separate legal personality (LPA s 11);

An indefinite lifespan if desired (LPA s 7, 97);

Restrictions on the participation of limited partners in management, allowing only “safe harbour” activities (LPA s 20, 31, Schedule 1) - see below; and

Income and losses flowing through the partnership into the hands of the individual partners for tax purposes. i.e. The partnership itself is not taxed in its own right. Note that you cannot claim more losses than the value of your capital contribution to the partnership. (ITA s HG).

Safe harbour activities include but are not limited to taking part in decisions about:

The wording of the partnership agreement and ongoing variations;

Whether to approve or veto any investment proposal, as set out in the Act;

Whether the general nature of the partnership should change; and

Termination of the partnership.

A complete list of safe harbour activities can be found in the Act which is available via the FBA website. (LPA Schedule 1).

Limited Partnerships are formed by registration with the Companies Office. An Overseas Limited Partnership must also register if it carries on business in New Zealand. The Registrar recognises that limited partners may not wish to publicly disclose their interest in a limited partnership. Details of limited partners are therefore treated as confidential and are not available for viewing by the public.

The Act sets out the minimum provisions of the partnership agreement (LPAs10). Surplus assets on liquidation are distributed to the partners in proportion to their capital contributions unless otherwise stipulated in the agreement (LPA s 95).

11.5.1 - Advantages of a Limited Partnership

The structure provides a win-win relationship between the active managers in running a business venture and the passive investors. The protections afforded to the passive investor are designed to encourage the necessary funding for general partners to succeed in their venture.

The above mentioned advantages of a traditional partnership continue to apply. Further benefits include separate legal identity and potential for the partnership to continue indefinitely as partners change. General partners have autonomy to manage the partnership on a day-to-day basis.

For the limited partners, there is the added benefit of limiting liability to the extent of investment in the partnership. This applies so long as they do not participate in the management of the partnership. Unless the partnership says otherwise, partner share in surplus assets in proportion to their investment if the partnership is wound up.

The limited partnership has become the preferred international venture capital and funds industries’ portfolio investment vehicle. This Act helps New Zealand to compete internationally to raise funds for business ventures.

11.5.2 - Disadvantages of a Limited Partnership

A limited partner has less protection than a minority shareholder would have in a company. The fiduciary duties of company directors are more onerous than the duties of general partners, potentially increasing risks.

As the income from the partnership increases, the tax benefits decrease to a point where it becomes detrimental for income to flow through the partnership into the tax returns of individual partners.

11.5.3 - Recommendation

Going back to the purpose of the Act, this structure is suitable to encourage sleeping partners to invest in business ventures. In the first stage of the venture, when there is likely to be a loss, there are tax benefits to having these flow through to individuals. Thereafter, it particularly suits investors whose marginal tax rate is lower than that of a company. This includes low income individuals, non-taxpaying partners (e.g. charities) and those who may have tax losses from other sources to offset against partnership income.

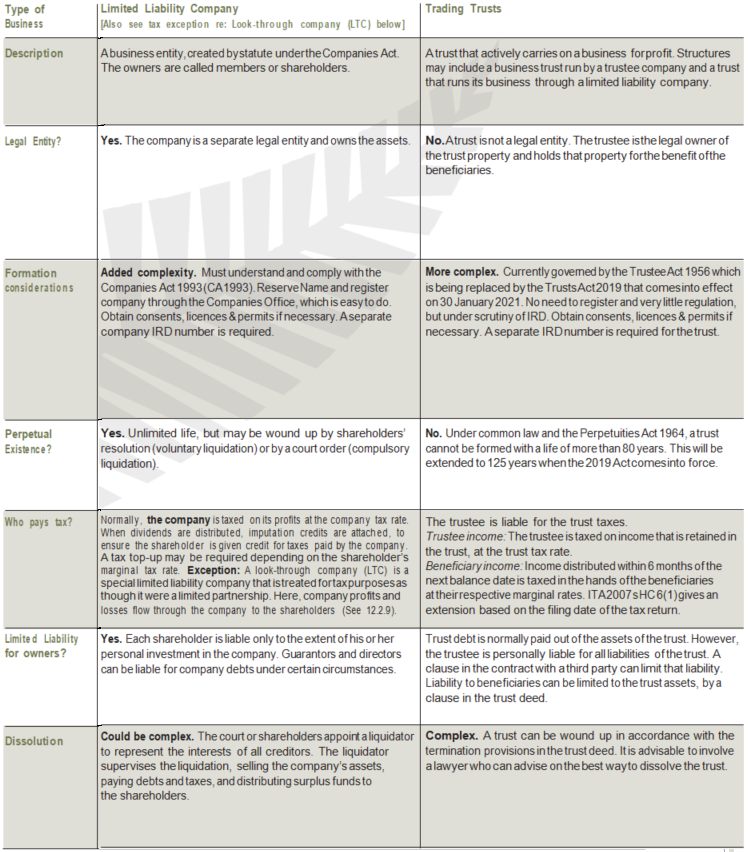

11.6 - Company Structures

A company is a separate legal person and must file a tax return (IR4) and pay tax in its own name. Look-Through Companies (LTCs) are companies that, for tax purposes only, are treated like partnerships. Even their tax returns are similar (IR7) (See Chapter 12).

11.6.1 - Advantages of a Company Structure

Companies provide a well-recognised and commercially acceptable structure for doing business

The owners of a company have the advantage of limited liability. If a company fails, the owners of that company will potentially only lose the value of shares they subscribed for in the company. In practice, the benefit of limited liability is often reduced as the individual directors and shareholders are often required to provide personal guarantees in respect of the company borrowings and trading activities

A company structure can accommodate multiple owners with differing interests in the business more easily than a partnership

A company structure provides the opportunity to benefit from the company tax rate of 28%, which is lower than the top individual marginal rate for income levels above $48.000.

A company structure is flexible. Changes in shareholding will not trigger deemed disposal of assets. However, shareholder changes can restrict the ability to carry forward imputation credits and tax losses (refer to Chapter 3).

Look-through companies (LTCs): These retain the commercial benefits of a company such as separate identity and limited liability. Losses are passed on to shareholders to set off against their profits as LTCs are effectively taxed as partnerships. There is a benefit for shareholders with a lower marginal tax rate than that of a company. Retained earnings can be distributed without “top-up” tax. There is no interest payable on overdrawn current accounts and capital gains can be passed on tax free to shareholders.

LTC can also be an attractive option for international investors.

11.6.2 - Disadvantages of a Company Structure

Various administrative requirements apply to companies. These include the requirement to keep a register of interests, a register of directors certificates, a register of directors, a share register; the requirements to pass directors and shareholders resolutions for certain transactions, keep minute books, produce annual financial statements, and to file company returns with the Companies Office.

The Companies Act 1993 also imposes stringent duties on directors of companies. For example, satisfying the solvency test for making a distribution to shareholders. Third parties, customers, suppliers, lenders etc can sue a director personally for breaches of those duties.

Compliance with the requirements of the Companies Act involves some additional cost. The fee for filing annual returns online, however, is nominal. (See 12.2.1)

Capital gains can only be distributed on the winding up of the company (unless the company is a qualifying company or LTC).

A company that can afford to do so should pay a shareholder employee a market-related salary to avoid possible challenge by the IRD (See 12.2.4). Also see 23.3.6 for the attributed personal services income rules. These limit but do not eliminate the opportunities to benefit from the company tax rate at higher income levels.

Companies are regulated to a higher degree than other business structures. The Companies Act 1993 has increased the rights of minority shareholders and imposes personal liability on directors in certain situations.

Look-through companies (LTCs): As a flow-through entity, an LTC does not benefit from the 28% tax rate.

Sale of shares, liquidation or exit from the regime are all deemed to be sale of underlying assets with possible tax consequences. After the transition rules expire, any tax losses brought forward will be forfeited when entering the regime. LTC status is revoked if the company is no longer eligible. The NZ Institute of Chartered Accountants (NZICA) wrote to the Minister of Revenue saying that members “have expressed their dismay at the complexity of and extensive compliance costs associated with, the LTC regime.”

11.6.3 - Qualifying Companies

This regime has been largely replaced by the new Look- through company. There is no longer a distinction between Qualifying Companies (QCs) and Loss Attributing Qualifying Companies (LAQCs). They are now all QCs. Certain tax benefits associated with QCs have been largely negated. They are taxed as flow-through entities and ordinary partnership rules apply to shareholders. However, losses are no longer able to be attributed to shareholders. Seek advice if you wish to move out of this regime, as there are likely to be tax consequences.

11.6.4 - Recommendation

A company structure is recommended for any commercial activity involving a potential exposure to commercial liability. This liability may include potential liability under the Fair Trading Act, the Resource Management Act and other liabilities imposed by statutes. If you are the director of a company, you should seriously consider:

obtaining directors liability insurance; and

holding your personal and investment assets in a separate structure that offers asset protection, such as a trust or company that is separate from your business

Since the company rate dropped to 28%, the ordinary company structure has become an even more attractive option. Do not convert to an LTC without seeking professional advice, as its suitability will depend largely on your circumstances.

11.7 - Trust Structure

On 30 July, the Trusts Act 2019 passed and comes into effect on 30 January 2021, replacing the Trustee Act 1956 and the Perpetuities Act 1964.

A trust is a legal promise by one party (the trustee) to hold and administer property for the benefit of other persons (the beneficiaries) in accordance with the wishes of a third party (the settlor) who settles the trust. The conditions upon which property in a trust is held should be set out in a trust deed.

Income in a trust will either be beneficiary income, if it is paid out to the beneficiaries within 6 months of the end of the income year in which it is earned, or trustee income, if it is retained in the trust.

Trustee income is taxed at the flat rate of 33%, while beneficiary income is taxed at the beneficiary marginal tax rates. Minor beneficiaries (i.e. beneficiaries younger than 16) are subject, in certain circumstances, to tax at the trustee tax rate (see Chapter 13 on Partnerships & Trusts).

Ordinarily, trusts are used to hold and protect personal assets (such as the family home) and investment assets (such as shares, commercial buildings etc). With some care, trusts can also be used to conduct a family owned business in a tax efficient manner. That is, trusts provide a flexible means of distributing earnings to beneficiaries, who in turn pay income tax at their lower marginal rates.

Example

Fred and Jack operate a dental business in partnership. There have been a number of ongoing business problems experienced by the partners. The partners agree to dissolve the partnership and Fred sells his share of the business to his family trust, which will run the business from the start of the new tax year. The trust registers for income tax and GST and Fred is now an employee of the trust. Fred takes out a market value salary and the remaining profits of the trust are distributed to beneficiaries on lower marginal rates.

In circumstances where good commercial reasons support the restructure and tax is seen as a merely incidental benefit, it is likely that the arrangement will be accepted for tax purposes. Specialist tax advice must be sought before such a trading structure is entered into.

11.7.1 - Advantages of a Trust Structure

Trusts provide opportunities for income splitting and utilisation of lower beneficiary marginal tax rates. However, distributions to minors under the age of 16 are taxed at 33% so that children are not used to lower family marginal tax rates.

Trusts provide protection for personal assets from creditors

Trusts are an excellent vehicle for family and estate planning, especially for matrimonial disputes, and when family members are on benefits, or beneficiaries are means tested

Trusts can provide for the smoother transfer of assets to family and provision for future generations

Trust structures are also flexible. Changes of trustees and the addition of beneficiaries will generally have no adverse tax effects. Also, trust deeds can allow trustees to resettle an existing trust into a new trust if circumstances require a resettlement but the tax effects will need to be weighed up.

11.7.2 - Disadvantages of a Trust Structure

Trusts can be expensive to set up and require ongoing administration

Income retained in a trust is taxed at the highest tax rate (33%)

When a trust debt is forgiven, unanticipated taxation can arise in certain circumstances

Resettlements of trusts may have tax consequences such as depreciation recovery, GST and accrual rules consequences; income tax on land transactions; and unutilised tax losses. When considering a resettlement, professional advice should be sought to assess the main tax implications.

11.7.3 - Recommendation

A trust structure is recommended where family assets are exposed to the commercial risks. Trusts can also be used to own and protect property and they remain an excellent vehicle for distributing income amongst several beneficiaries.

Summary