Chapter 17 – Provisional Tax

17.1 Overview

Provisional tax is a means of paying tax on income, that is not fully taxed at source via PAYE or other withholding payments.

There are several options available and effective management of your provisional tax liabilities can help with your cash flow and save you literally thousands of dollars.

Provisional tax is not an extra tax. It is a means by which taxpayers are required to meet their income tax liability by paying instalments progressively throughout the year. The Law offers a number of options (“methods”) from which a taxpayer may choose to satisfy this tax liability.

These are explained in this chapter. From 1 April 2018, the accounting income method (AIM), gives smaller businesses a new pay-as-you-go option for provisional tax.

To ensure that taxpayers comply with their obligations to pay provisional tax, a series of penalties apply to late payments and under-payment of provisional tax. Additionally, an interest charge known as “use of money interest” may apply to both overpayments and underpayments of provisional tax. Even if you comply with the law by paying your instalments on time, based on an accepted method for calculating the tax, you may still end up paying use of money interest (UOMI -See 17.2.7.3). However, recent improvements to the regime will reduce and in some cases eliminate UOMI for taxpayers who choose and comply with the Standard uplift method.

17.2.1 Who Has to Pay Provisional Tax?

17.2.2 What is Residual Income Tax?

17.2.3 Due Dates

17.2.4 How Much Provisional Tax to Pay?

17.2.4.1 Standard Option

17.2.4.2 The Accounting Income Method (AIM)

17.2.4.3 The Estimation Option

17.2.4.4 Ratio Option

17.2.5 New Provisional Taxpayers

17.2.6 Provisional Tax Discount for New Businesses

17.2.7 Penalties

17.2.7.1 Late Payment Penalty (TAA s 139A-139B)

17.2.7.2 Lack of Reasonable Care

17.2.7.3 Use of Money Interest (UOMI)

17.2.7.4 Safe Harbour Provisions

17.3.1 Plan Ahead!

17.3.2 Provisional Tax Obligations

17.3.3 Estimation

17.3.4 Safe Harbour

17.3.5 Use of Money Interest/Voluntary Payments

17.3.6 Before the Final Provisional Tax Due Date!

17.3.7 Pooling of Provisional Tax Payments

17.3.8 Provisional Tax Intermediaries

17.2 Application

17.2.1 Who Has to Pay Provisional Tax?

If you had more than $2,500 of tax to pay at the end of the year from your last income tax return, you’ll have to pay provisional tax the following year.

You may also elect to be a provisional taxpayer if you have a reasonable expectation that your residual income tax will be $2,500 or more during the year.

17.2.2 What is Residual Income Tax?

Residual income tax (“RIT”) is the key figure used to determine any provisional tax liability. In other words, if RIT is $2,500 or more in any tax year, you will be required to pay provisional tax in the following year.

RIT is calculated as the amount of tax to pay on your taxable income (See 2.1), less any PAYE deducted and any other tax credits you may be entitled to other than Working for Families Tax Credits.

Example

Let’s say your company has gross taxable income of $56,000 and deductible expenditure of $16,000. No taxes have been deducted at source. In this case, the total net income is $40,000 and the residual income tax (RIT) is $11,200 (applying the company tax rate of 28%).

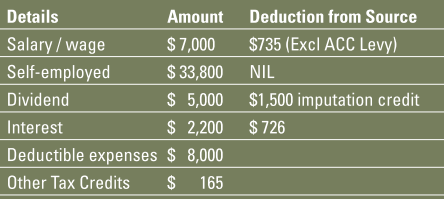

Doe is a freelance journalist with several sources of income including part time employment from which PAYE is deducted. Income and expenditure for the year are as follows:

Complete the following steps to establish Doe’s RIT:

$40,000

$6,020

($2,961)

($ 165)

$ 2,894

Total Net Income:

($7,000+$33,800+$5,000+$2,200-$8000)

Tax Using Marginal Tax Table – See 2.1.1:

Less PAYE and other source deductions:

($735+$1,500+$726)

Less tax credit:

RIT

Doe’s RIT for the year is $2,894. As this is more than $2,500, Doe is a provisional taxpayer for the following tax year and must pay provisional tax in the following year to avoid penalties and interest.

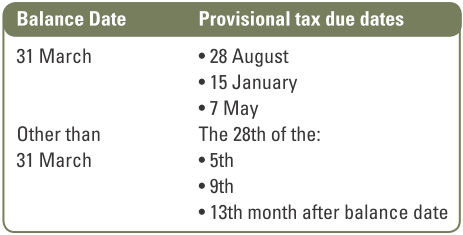

17.2.3 Due Dates

Provisional tax is generally payable in instalments during any income tax year, calculated according to one of the following options:

It can be paid on the basis of prior year income plus an uplift factor; or

A taxpayer may estimate the amount of provisional tax payable for the year

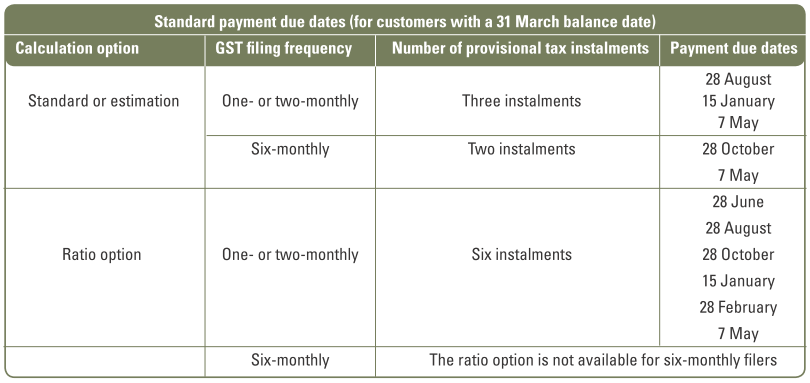

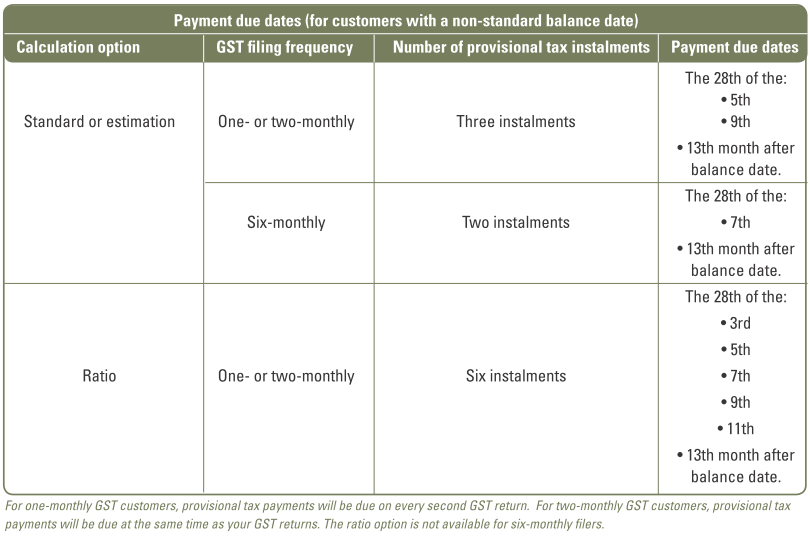

Due dates for provisional taxpayers who are not registered for GST:

Provisional taxpayers who are registered for GST are able to pay both taxes at the same time using a combined GST and provisional tax return (GST103B) in the months when provisional tax is due. This means only having to complete one form and make one payment during these months. For GST-registered provisional taxpayers, the filing dates are shown in the tables below.

17.2.4 How Much Provisional Tax to Pay?

Provisional taxpayers have the following options available when deciding how much provisional tax to pay for any income year.

The standard method allows provisional tax payments to be based on the RIT of previous years with an uplift to take any growth into account. There is a new accounting income method, an estimation option, a ratio option and soon-to-be accounting income method (AIM).

These are all discussed below.

17.2.4.1 Standard Option

This is the default option used by the IRD unless you choose an alternative method. It is calculated on 105% of the previous year’s residual income tax (RIT) or, if that year’s income tax return has not yet been filed, on 110% of the RIT for the year before that.

Example

Doe’s RIT for 2016-17 was $2,894 (See 17.2.2). Doe files GST returns 6-monthly and has a balance date of 31 March. Doe therefore pays 2017-18 provisional tax in two equal instalments on 28 October 2017 and 7 May 2018. The instalment amounts are calculated as: ($2,894 x 105%) /2 = $1,519.35.

Example

Assume Doe’s 2016-17 income tax return had not been filed by 28 October 2017 and the RIT for the 2015-16 year was $2,820.

The first instalment for 2017-18 could be based on ($2,820 x 1.1) /2 = $1,551. This is more than could have been paid had the 2017 tax return been filed on time ($1,519.35).

Assuming $1,551 is returned on 28 October 2017, the amount payable on 7 May 2018 is based on the RIT of the most recently filed 2017 tax return ($2,894) less previous instalments paid, as follows: ($2,894 x 105%) - $1,551 = $1,487.70.

17.2.4.2 The Accounting Income Method (AIM)

From 1 April 2018, taxpayers with an annual turnover of up to $5 million, who use approved accounting software, are able to choose this method to calculate and pay provisional tax based on their actual income. The calculations are made by the software based on adjusted information for the accounting period. Payments are made:

monthly for businesses registered for monthly GST returns; and

two monthly for businesses who file GST two- or six- monthly and for those not registered for GST.

By having AIM information generated by real-time software, it is the intention for the calculation and payment of provisional tax to become part of running the business instead of being an extra process. To be approved, software will need to comply with IRD specifications and IRD will be able to audit any software. MYOB, Reckon and Xero were the first packages to gain IRD approval.

17.2.4.3 The Estimation Option

The standard option referred to above can be disadvantageous when your current year income is expected to be less than your prior year’s income tax. In this case, you could choose to estimate your provisional tax payable for the current year downward.

All provisional taxpayers may choose to estimate their current year’s RIT and pay provisional tax based on that estimate. A taxpayer choosing to estimate must by any instalment date file an estimate or revised estimate with Inland Revenue (form IR309).

Example

Your current year income may be expected to decline significantly from the prior year. In this case, you could consider using the estimation method to reduce provisional tax payable in the current year.

You can change from the standard option at any time up to your final instalment date and you can estimate your provisional tax as many times as necessary up to and including your last payment due date for the tax year. Each estimate must, however, be fair and reasonable. If your estimated RIT is lower than your actual RIT for that year, you’ll be charged interest on the underpaid amount.

17.2.4.4 Ratio Option

Eligible GST-registered taxpayers also have an option to calculate provisional tax instalments based on a percentage of their previous year’s GST taxable supplies (sales). This is called the ratio option.

The IRD will normally calculate the taxpayer’s ratio percentage using the following formula:

Note: Taxable supplies are reduced by your asset adjustment (See 20.3.17).

Having calculated your ratio percentage, the IRD will inform you what it is.

This is then applied to the previous period’s GST taxable supplies to arrive at the provisional tax payable. For example, adjusted RIT for previous year is $100,000. GST taxable supplies for previous year is $1.2 million. The ratio is 100,000/1.2 million x 100 = 8.33%. The taxable supplies for the past 2 months in the GST return are 210,000. Therefore the provisional tax payable for this instalment is

$210,000 x 8.3% = $17,430.

The ratio option better reflects cash flow and uses this to work out how much provisional tax is due. This may suit businesses that have fluctuating income during the year. Those wishing to adopt it must apply before the end of the tax year and meet the following criteria:

They must be operating a business (other than a partnership) and have been GST registered for all of the previous income year, and part of the income year prior to that.

RIT must be in the range from $2,500 to $150,000

GST returns are filed monthly or two-monthly. Those who wish to use the ratio option but are currently on six monthly filing will need to change to one or two monthly filing.

You should consult your tax advisor if you change your balance date to ensure correct amounts are paid at required instalments.

17.2.5 New Provisional Taxpayers

An exception to the rule that provisional tax is payable in 2 or 3 equal instalments, is the case of a new provisional taxpayer. A new provisional taxpayer is a natural person or a company that has only begun business in the current year and did not conduct business in the four preceding years.

A natural person (other than a trustee) is also a new provisional taxpayer if the RIT did not exceed $2,500 in the four preceding years, but where current RIT exceeds

$50,000 for the income year, and the taxpayer ceased to derive employment income and started to earn gross income from a taxable activity.

If you think this situation applies to you then consult your advisor. It may be that you are liable to pay provisional tax and interest.

17.2.6 Provisional Tax Discount for New Businesses

To encourage self-employed people and those who receive income from partnerships to pay provisional tax in their first year of business, rather than the following year when it is due, the IRD offer a 6.7% discount on the amount payable.

The discount is calculated on the lesser of:

the amount of tax paid for the income year before balance date; or

the amount of terminal tax payable for the income year.

Traditionally, self-employed take a big tax hit in the second year of business (when both terminal tax and provisional tax are due) which is often not fully budgeted for.

Early payment (with the discount sweetener) could give the newly self-employed person a better chance of avoiding a false sense of cash flow availability down the track.

17.2.7 Penalties

17.2.7.1 Late Payment Penalty (TAA s 139A-139B)

If the correct provisional tax payments are not made by the due date, an instant 1% late payment penalty will apply with a further 4% 7 days later. Note: A further 1% monthly penalty was scrapped from 1 April 2017. (See Chapter 24). Failing to pay your provisional tax on time is simply throwing money away unnecessarily.

17.2.7.2 Lack of Reasonable Care

With the repeal of the underestimation penalty and associated provisions, taxpayers are now required to take ‘reasonable care’ when estimating each instalment.

As a result of the enactment of the reasonable care test, a number of changes have arisen:

If a taxpayer pays more than last year’s RIT they will be deemed to have taken reasonable care

Taxpayers who expect to have RIT in excess of $35,000 are no longer compelled to estimate their provisional tax liability (but should manage their use of money interest exposure)

Where a taxpayer does not take reasonable care in providing an estimate they will be liable for a 20% penalty (refer to Chapter 24)

WARNING!!

Ensure that you calculate your current year provisional

tax correctly. The financial costs for misinterpreting your obligations can hurt. Even if you are not obliged to make a provisional tax instalment, expensive use of money interest charges (see discussion below) can still apply.

17.2.7.3 Use of Money Interest (UOMI)

The IRD may charge interest on underpaid provisional tax and pay interest to those who have overpaid. This interest is known as “use of money interest” (UOMI). The interest is calculated on the difference between the actual RIT for the year and the provisional tax paid for that year. The UOMI is determined by:

• dividing your actual (assessed) RIT for the year by the number of instalments and

• comparing provisional tax actually paid at each instalment date with the provisional tax that should have been paid by then.

From April 2017, UOMI is now charged as follows:

Nil if you satisfy the Safe Harbour provisions (See 17.2.7.4); or

Calculated from the date of your final instalment, if you choose the standard uplift method and pay your first two instalments correctly, but have a current year RIT greater than $60,000; or

Calculated retrospectively from your first instalment date in all other cases.

UOMI has been removed for the first two provisional instalments for all tax payers who use the standard uplift method to pay provisional tax.

UOMI keeps accruing until the tax owing is paid. If you have overpaid, the IRD will pay you interest up until the date your overpayment is refunded or transferred to settle other amounts owing to the IRD. If you elected to be a provisional tax payer, paid more than $2,500 before your final instalment date and your RIT turned out to be $2,500 or less, you may also be eligible to be paid interest on your overpaid tax.

From 29 August 2019 UOMI interest rates are:

Charged by the IRD on underpayments: 8.35%

Paid by the IRD on overpayments: 0.81%

Interest you pay is generally tax-deductible, while interest paid to you is taxable. Anti-avoidance rules apply to prevent manipulation for the purpose of avoiding UOMI and in particular, the use of associated persons for such purposes.

17.2.7.4 Safe Harbour Provisions

Provisional taxpayers are not charged (or paid) UOMI if :

they have an RIT in the current tax year of less than $60,000, known as the Safe Harbour threshold; and

they choose the standard uplift method; and

they pay instalments correctly based on their last assessment; and

all associated persons use the standard uplift method or the GST ratio method to calculate provisional tax.

This now applies to non-individuals as well as individuals.

17.3 Practical Hints

17.3.1 Plan Ahead!

Diarise your provisional tax payment dates and contact your tax advisor at least a week prior to the date to discuss payment options and amounts.

17.3.2 Provisional Tax Obligations

If you are unclear about your provisional tax obligations you should consult a professional advisor. Penalties for non-compliance, including innocent mistakes, can be severe.

17.3.3 Estimation

If your provisional tax for the current year is expected to be significantly lower than the provisional tax paid last year, consider using the estimation option to reduce your current year provisional tax payments.

17.3.4 Safe Harbour

To benefit from these provisions, if your RIT is below the Safe Harbour threshold, make provisional tax payments based on the standard uplift (safe harbour) method and pay these on time.

17.3.5 Use of Money Interest/Voluntary Payments

Always consider your exposure to use of money interest. If you fail to make the correct instalment payment on time, it could cause you to be liable for UOMI from the date of your first instalment. If you are liable for interest, consider making “voluntary” top-up payments of provisional tax to reduce the UOMI due. Make it clear to the IRD that you are not making an estimate but are merely making a voluntary additional payment. This can be done at any date after the first payment date.

17.3.6 Before the Final Provisional Tax Due Date!

Ensure that you review your expected year-end results before your final provisional tax instalment date! In particular consider whether the provisional tax paid to date when combined with the proposed final instalment will be sufficient to prevent expensive use of money interest charges. If profit projections for the current year exceed those of last year, this will become an important provisional tax issue.

17.3.7 Pooling of Provisional Tax Payments

Taxpayers are able to pool their provisional tax payments with other taxpayers and as a result, provide under payers of provisional tax and over payers of provisional tax with a more efficient rate of interest. That is, provisional taxpayers who have contributed more than required to the pool will earn interest at better than the IRD rate (at the time of printing) of 1.62% for over payments. Taxpayers who have contributed less than their required amount to the provisional tax pool will be charged interest at less than the current rate for under payments of 8.27%. A number of tax agents/accountants are now offering provisional tax pooling to clients.

17.3.8 Provisional Tax Intermediaries

Use of money interest charges and certain penalties can be reduced by the use of tax payment intermediaries authorised by the IRD.

These intermediaries effectively sell overpayments of provisional tax to taxpayers who have underpaid, giving taxpayers:

the ability to defer tax payments for up to eleven months;

higher interest on tax overpayments;

lower interest on tax underpayments;

earlier tax refunds;

See your financial advisors about these opportunities to reduce the Taxman’s cut.