Chapter 19 – Fringe Benefit Tax

19.1 Overview (ITA ss RD 25 - RD 63)

Fringe benefit tax (FBT) was introduced to tax non-cash benefits provided to employees or associates of employees. These rules also apply to non-cash benefits provided to shareholder employees and their associates.

The fringe benefit tax rules apply to a range of benefits. Principally these include:

Providing the private use or availability for private use of a motor vehicle to an employee. (Private use includes travel between home and work in most instances)

Employer-provided car parks

Employment related or low interest loans by an employer

Other goods and services provided by an employer at a price lower than the market value

Various insurance premiums for example medical insurance and certain superannuation contributions

Any benefit of any other kind whatsoever, although there are some specific exemptions, such as Health and Safety related obligations on or off premises

The definition of fringe benefit is wide and FBT is a standard area for close review in a tax investigation. Inland Revenue Auditors frequently find mistakes in this area.

19.1 Overview (ITA ss RD 25 - RD 63)

19.2 Application

19.2.1 Attributed Benefits

19.2.2 Non-Attributed (Pooled) Benefits

19.2.3 Short-form Alternate Rate Calculation

19.2.4 Full Alternate Rate Option

19.2.5 Calculating FBT Using the Full Alternate Rate Option

19.2.6 Major Shareholder-Employees

19.3.1 Quarterly, Annual or Income Year

19.3.2 GST Output Tax

19.3.3 Motor Vehicles

19.3.3.1 Work Related Vehicles

19.3.3.2 Vehicles Stored on the Employer’s Premises

19.3.3.3 Emergency Call

19.3.3.4 Other Days Not Liable

19.3.3.5 Out of Town Travel

19.3.3.6 Calculating the Value of the Benefit - Motor Vehicles

19.3.3.7 Travel between Home and Work

19.3.4 Car Parks

19.3.5 Low Interest Loans

19.3.6 Tax Returns

19.3.7 Non-Cash Benefits to Shareholder Employees

19.3.8 Subsidised or Free Goods and Services

19.3.9 General exemption from FBT

19.4.1 Motor Vehicle Exemptions

19.4.2 Motor Vehicle Record Keeping

19.2 Application

FBT is levied on employers on the value of fringe benefits provided to employees. The term “employees” is defined widely and includes past, present and future employees. The term employee also includes shareholder employees and directors of a company.

FBT is calculated on the value of the benefit provided. FBT paid by an employer is generally tax deductible including the GST paid on the fringe benefits supplied.

Employers may choose to pay a single flat FBT rate of 49.25% without performing any attribution calculations as described in the following sections. This applies whether you file quarterly or annually.

19.2.1 Attributed Benefits

A benefit will be attributable to an employee if the benefit is principally assigned, used or available for use by that employee during the respective FBT period.

The legislation requires the following fringe benefits to be attributed to the employee who benefited from them.

motor vehicles used or available for private use (other than pool vehicles)

affected car parks

employee loans. From 1 April 2019 an overpayment of wages is no longer treated as a loan subject to FBT

following benefits with a total taxable value of $1,000 or more (per category, per year, per employee):

subsidised transport

contributions to sick, accident or death funds

specified insurance premiums or any contribution to any insurance fund of a friendly society

contributions to any superannuation scheme

any other benefits provided with a taxable value of $2,000 or more (per year, per employee)

EXAMPLE

An employer who provided an employee with medical insurance with a taxable value of $300 per quarter would be required to attribute that benefit to the employee recipient ($300 x 4 quarters = $1,200, which is more than $1,000).

EXAMPLE 2

An employer provides a motor vehicle to employee A for quarters 1 to 3, but then employee B becomes the principal user in quarter 4. Under these circumstances, the employer would be required to attribute the value of the vehicle over quarters 1 to 3 to employee A, and the value in quarter 4 to employee B.

19.2.2 Non-Attributed (Pooled) Benefits

Any benefits that are not attributable to an employee must be pooled. For example, a category of benefits with a taxable value below the monetary attribution thresholds, or a motor vehicle with no predominant user. The FBT rate for pooled benefits is 42.86% (or 49.25% for major shareholder-employees).

Benefits that must be pooled include those that are not referred to in 19.2.1 above.

There is also a special rule that subsidised transport can be pooled provided all employees have the same or similar entitlement to the benefit.

Benefits provided to former employees or low-interest loans provided by life insurers to policyholders must also be pooled. This is because the employer will not have access to the recipient’s income information.

Employers can choose to attribute benefits below the threshold should they wish. However, if any benefits below the monetary threshold are attributed, then all benefits in that category must be attributed. In other words, an employer cannot decide to attribute an insurance premium of $500 per year only to low-income employees and not to all other employees.

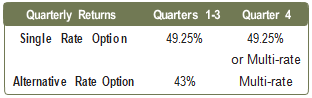

19.2.3 Short-form Alternate Rate Calculation

This year-end “washup” option may be chosen by those who file FBT quarterly or annually. If you paid FBT at the alternate rate of 43% in any of the first three quarters, you must use either this or the full alternate rate calculations in the fourth quarter.

This option allows all non-attributed benefits to be taxed at a flat rate of 42.86%, or 49.25% where one or more recipients is a major shareholder-employee. You may need two pools for non-attributed benefits in this situation (See 19.2.2). This option suits employers who mainly provide attributed benefits to employees earning $70,000 or more.

In the 4th quarter or annual return, employers simply add all attributed benefits provided to employees together and calculate the FBT on the combined figure at 49.25%. See 19.3.1 for filing details.

The non-attributed benefits are calculated the same way as they are under the full alternate rate option.

19.2.4 Full Alternate Rate Option

The full alternative rate calculation is designed to reduce over-taxation of attributed fringe benefits provided to employees who are not on the top marginal tax rate.

Under this option, you perform a separate calculation for each employee who has received attributed benefits and the FBT rate depends on the fringe benefit-inclusive cash remuneration (FBICR) received by each employee (See 19.2.5).

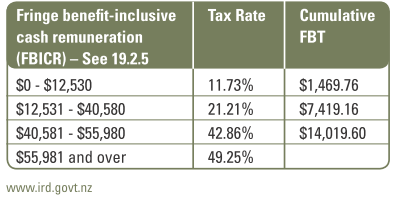

The FBICR rates are:

You still have the option of paying fringe benefit tax of 49.25% on attributed fringe benefits rather than applying the alternate rates.

Under the full alternate rate option, employers paying FBT on a quarterly basis must either:

elect to pay FBT at either 42.86% or 49.25% for the first three quarters, and in the final quarter pay FBT applying the full alternate rate option; or

elect to pay FBT at 49.25% for the first three quarters, and in the final quarter elect to pay FBT at 49.25% or apply the alternate rate process.

Employers paying FBT on an annual or income year basis must pay FBT either at the rate of 49.25% or applying the full alternate rate option.

The above rules effectively provide that an employer either pays FBT at a single rate of 49.25% or attributes fringe benefits to individual employees and pays FBT at rates based on the employees’ marginal tax rates. The first step in the calculation is to determine which employee received the benefit. This is called attribution. Fringe benefits that are not attributed to an individual employee must be pooled and are taxed at a single rate of 42.86% or 49.25% if one or more recipients is a major shareholder-employee (but see 19.2.6 below).

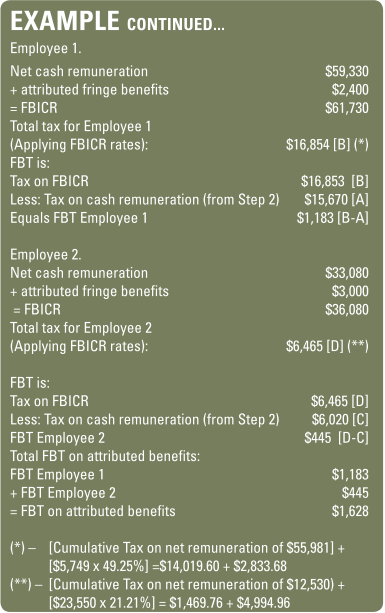

19.2.5 Calculating FBT Using the Full Alternate Rate Option

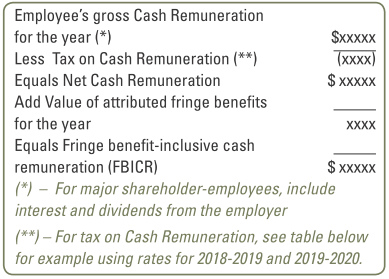

The full alternate rate option is entirely different to the previous FBT computations. Attributed benefits are taxed on a sliding scale up to 49.25% depending on the employee’s fringe benefit-inclusive cash remuneration (FBICR). FBICR is calculated as follows for each employee:

The FBICR is then taxed according to the table in 19.2.4 to obtain the FBT on attributed benefits. To this, the FBT on pooled benefits is added to obtain the total FBT liability. This is demonstrated in more detail, applying the following steps:

Step 1: Calculate the cash remuneration of each employee: This includes wages, salary, bonuses, commissions and any other cash payments.

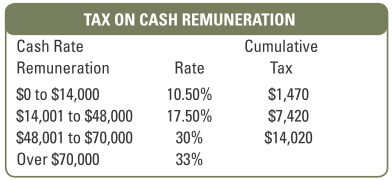

Step 2: Calculate the net cash remuneration of each employee: To do this you need to deduct taxation using the current individual tax rates. Rates are based on effective marginal rates (See 2.1.1) as follows:

Step 3: Determine the ‘Fringe Benefit-Inclusive Cash Remuneration’ (FBICR): Add the value of just the attributed fringe benefits (not the pooled benefits) to the net cash remuneration calculated in Step 2. The resulting figure is the ‘Fringe Benefit-Inclusive Cash Remuneration’ (FBICR) that is taxed according to the table in 19.2.4 above).

Note: Rates for attributed benefits are as in the FBICR table under 19.2.4.

A calculation needs to be made for all employees provided with attributed benefits to determine the total FBT payable for all attributed benefits.

Step 4: Calculate the FBT liability for pooled benefits: All benefits that have not been attributed must be pooled. To calculate the FBT liability on these benefits, simply add together the taxable value of all benefits that have not been attributed and calculate the FBT liability.

There are two rates applicable depending on whether a major shareholder-employee or an associate is one of the recipients (and it is possible to create two separate pools):

FBT = Total taxable value of all pooled benefits x 42.86% (When no major shareholder employee or associate is one of the recipients)

FBT = Total taxable value of all pooled benefits x 49.25% (When a major shareholder-employee or an associate is one of the recipients.)

Step 5: Calculate total FBT payable: Total FBT payable equals the sum of:

Total FBT for attributed benefits

Plus total FBT for pooled benefits

Less FBT assessed in quarters 1-3 (quarterly filers only)

19.2.6 Major Shareholder-Employees

There are special rules for major shareholders who are also employees. In general terms, a major shareholder is a person who directly or indirectly owns or controls 10% or more of the ordinary shares of a close company.

The cash remuneration for a major shareholder includes remuneration, dividends and interest derived from the employer or a related employer (that pays remuneration to the shareholder employee in question). Cash remuneration also includes any amount of income attributed under the attributed personal services income rules as referred to in Section 23.3.6.

Shareholder-employees who are income year filers can elect the flat rate of 49.25%, or the alternate-rate option. The options for attributed income don’t apply to them as the due date for this return is aligned with the end of year tax date of the employer and not all necessary income information would be known by this date. In these situations, employers may either:

elect to pay FBT at 42.86% and carry out the alternate rate calculation in the relation to those benefits in the following income year; or

elect to pay FBT at 49.25% on attributed benefits, in which case no subsequent alternate calculation is required.

Any pooled benefits where one or more of the employee recipients is a major shareholder-employee (or an associate who received the benefit other than as an employee) must be taxed at 49.25% rather than the 42.86% pooled rate. However, employers are able to create two distinct pools. One pool can be taxed at 49.25% for those benefits that include a major shareholder-employee as a recipient, and the other taxed at 42.86% for any benefits only received by other employees.

Note: For a major shareholder-employee (or an associated person, where the fringe benefit is not received as an Employee) the single rate option (formerly flat rate) applies to non-attributed fringe benefits that they receive.

The benefits received by associates of a major share holder - employee, who are not themselves employees, must be added to the calculation of FBT liability for the major shareholder-employee concerned.

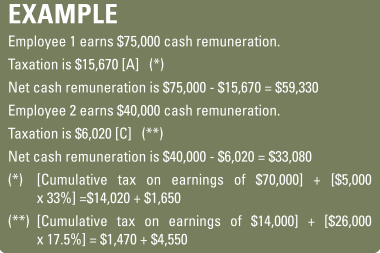

EXAMPLE

A manufacturer provides the following benefits to its five employees and one major-shareholder-employee:

(a) Free goods with a taxable value of $400 to all employees over the year (except the major shareholder-employee)

(b) Medical insurance valued at $200 per quarter to all employees

With benefit (a), the employer does not need to attribute the benefit to each of the employees since the benefit does not exceed the annual allowance of $22,500. This is based on the assumption that employees did not receive more that

$300 worth of goods in each quarter (see 19.3.9 below). If the goods had exceeded the $300 per quarter then the employer can choose to either attribute the benefit to each employee or apply a flat rate of 42.86% pooled rate.

With benefit (b), the employer can choose either to attribute the medical insurance to each employee or apply the 49.25% pooled rate ([$200 x 4 quarters] x 6 employees x 49.25%).

This choice will largely be influenced by the remuneration of the employees concerned.

19.3 Practical Issues

19.3.1 Quarterly, Annual or Income Year

Employers who provide fringe benefits must file FBT returns with the IRD. These returns can be completed either quarterly, annually or on an income year basis.

For employers filing FBT returns each quarter, the return period and due dates are:

Filing FBT Quarterly

If you pay FBT quarterly at the single rate of 49.25% in all of the first three quarters, you have three choices in the fourth quarter. These are:

pay FBT at the 49.25% single rate. If you choose this option you must use this rate for all benefits provided during the year;

using the short-form alternate rate calculation; OR

using the full alternate rate calculation.

If you paid FBT at the alternate rate of 43% in any of the first three quarters, you must use one of the alternate rate calculations in the fourth quarter.

Employers with PAYE deductions and employer superannuation contribution tax (ESCT) deductions up to $1 million, can pay FBT on an annual basis. Annual FBT return must be filed by 31 May that first follows the end of that year.

19.3.2 GST Output Tax

15% GST output tax is calculated based on 3/23 of the value for FBT purposes. The GST on fringe benefits is included in the FBT return for the period in which the benefits are provided.

EXAMPLE

If the taxable value of goods provided free in the quarter ending 30 June was $3,000, a GST output tax adjustment of 3/23 x $3,000, that is $391, is required to be returned in the July FBT return.

Completing the return

Step 1: Take the total taxable value of all fringe benefits from Box 3 of your FBT return. (Note, this is the benefits, not the FBT itself.)

Step 2: Deduct the value of benefits which are exempt or zero-rated for GST purposes such as:

low-interest loans and other financial services

international travel

contributions to employee superannuation and life insurance policies.

This is the fringe benefits amount that is liable for GST.

Step 3: Multiply the Step 2 result by 3/23.

This is the GST adjustment to include in your FBT return and must be entered in:

Box 7 of the quarterly FBT return (IR 420) for quarterly filers

Box 6 of the annual FBT return (IR 422) for annual filers

Box 6 of the income year FBT return (IR 421) for income year filers.

19.3.3 Motor Vehicles

FBT is calculated on the number of days the vehicle is used or available, for private use. If the motor vehicle is available for the private use for any part of the day, then that whole day is counted as being subject to FBT even where the vehicle was not actually used for private purposes. Note that private use includes travel between home and work.

From the 2017-18 income year, a close company may elect to opt out of the FBT rules if it has only 1 or 2 motor vehicles available for private use by its shareholder-employees, and provides no other fringe benefits. The election must be made by the due date for filing your tax return in the year the vehicle is acquired or first used in your business. The motor vehicle expenditure rules then apply and you must adjust the expenditure for private use. Once you have opted out for a vehicle, you can’t return to using the FBT rules for it.

Fringe benefit tax payable on motor vehicles can be reduced in the following circumstances and see 5.2.3.1.

19.3.3.1 Work Related Vehicles

Where a motor vehicle qualifies as a work related vehicle, then travel in that vehicle, including travel between work and home, will be exempt from FBT (any other private use will still be subject to FBT). To qualify as a work related vehicle, the following requirements must be satisfied:

The principal design of the vehicle cannot be for carrying passengers.

The employer’s name or logo is permanently and prominently displayed on the vehicle.

The employer has notified employees in writing that the only private use of the vehicle is limited to:

travel between home and work;

travel in the course of and as a condition of the employee’s duties

private travel incidental to business travel

The employer must carry out quarterly checks on each vehicle for which this exemption is claimed to ensure that the restriction is being adhered to.

Vehicles that can qualify include:

Utility Vehicles (including extra cabs and double cabs).

Light pick-up trucks.

Vehicles with rear doors that are permanently without rear seats such as vans, station wagons, hatchbacks, panel vans, and four-wheel drives. This also applies if the rear seats have been welded down or made unusable because of a fixture such as shelving covering the rear seat area.

Taxis (including sedans and station-wagons).

Minibuses. That is, vans with three or more rows of permanent (not collapsible) seats capable of carrying at least two adults each.

On any day when all of these requirements are met, the vehicle will not be subject to FBT.

The IRD frequently encounter business taxpayers who misunderstand the work related vehicle provisions. Often shareholder employees will purchase vehicles and have them sign written. The vehicle will be used extensively for private running. In these circumstances, many business taxpayers fail to pay for the fringe benefit tax on the mistaken belief that the vehicle is a work related vehicle. In these situations, the IRD will often collect FBT for the current year and the prior three years, plus impose penalties ranging between 20% to 40% plus use of money interest.

19.3.3.2 Vehicles Stored on the Employer’s Premises

Any vehicle that is stored on the business premises is not subject to FBT if the vehicle is not available for private use.

19.3.3.3 Emergency Call

A partial exemption from FBT is available if the motor vehicle is used for an emergency call. An emergency call is where an employee provides services at the request of the employer or client or customer between 6pm and 6am on any weekday, or anytime on Saturday, Sunday or any statutory holiday. However, the services must be essential to the operation of any plant or machinery of the employer, or any client or customer of the employer, or be essential to the maintenance of any service provided by a public or local authority or in relation to any business that provides any energy or fuel to the public. Also, where the emergency call relates to the health or safety of any person then none of the above time related restrictions apply.

19.3.3.4 Other Days Not Liable

If a vehicle is unavailable for at least a complete 24-hour period, for example the vehicle is broken down, then an exemption can be claimed.

19.3.3.5 Out of Town Travel

An exemption also applies where an employee is required to be away from home on business for 24 hours or more. Each day the employee is away is not included in the calculation of the number of days the vehicle is available for private use.

It is important to note that in order to calculate the “number of days available for private use” you must deduct the number of exempt days in a quarter from the actual number of days in a quarter.

EXAMPLE

There are 92 days in the December quarter. If the motor vehicle is exempt for 22 days, then it will be available for 70 days, i.e. 92 less 22.

For taxpayers on an annual basis simply deduct the exempt days from 365.

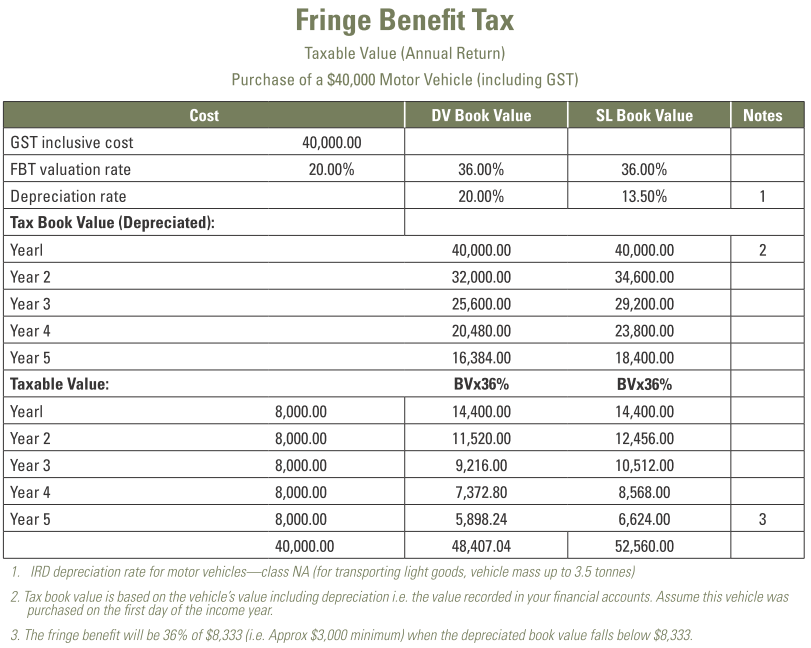

19.3.3.6 Calculating the Value of the Benefit - Motor Vehicles

FBT on vehicles may be calculated on either the cost price or the tax book value.

Cost price includes GST and any initial costs of getting the vehicle on the road, as well as extras such as a CD player, sun-roof or tow-bar. It does not include items such as registration and WOF. Trade-in values should not be subtracted from the cost price.

The taxable value of a motor vehicle for FBT purposes is calculated on:

5% of the GST inclusive cost of the vehicle, per quarter; or

20% of the GST inclusive cost, if FBT is being returned annually

Tax book value is the cost of the vehicle if acquired after the beginning of the tax year and for subsequent years it is the vehicle’s original cost price less the total accumulated depreciation (as per the financial accounts). This option has a minimum value of $8,333 that must be used once the tax book value has depreciated to below this amount. This equates to a benefit of approx $3,000 per annum for an employee ($8,333 x 36%).

The FBT annual rate of 36% (or 9% quarterly) costs an employer more in the initial years compared to the cost price option. However, it will benefit employers who keep their vehicles for five years or more. If this option is chosen it must be applied for at least five years or until the vehicle is no longer owned or leased.

Whichever option is used, the value is then apportioned by the number of days available for private use.

EXAMPLE

A taxpayer used the cost method of valuing vehicles and files a quarterly FBT return. The original cost price including GST of the vehicle was $40,000. The number of days available for private use was 70 days in the quarter

calculation: 70 days/90 days x $40,000 x 5% = $1,556

The value of the fringe benefit is $1,556 in the quarter. FBT on this would be $771 ($1,556 x 49.25%)

The amount of the fringe benefit can be reduced where the employee makes a contribution towards the fringe benefit value.

EXAMPLE

Where the employee contributed $200 in return for having the use of the vehicle, then this amount will be deducted from the taxable value of the fringe benefit. In the above example this would reduce the taxable value from $1,556 to $1,356. Accordingly the fringe benefit tax applicable would also be reduced from $762 to $668.

19.3.3.7 Travel between Home and Work

Your business set-up is important where travel deductions are concerned. The IRD have recently issued a draft statement on whether or not you can take a deduction on the above. Generally regarded as private expenditure but IRD do allow a deduction in the following circumstances:

the vehicle is essential for transport of goods or equipment necessary for income earning activities, e.g. because of their bulk;

you carry on an “itinerant” occupation and home is your operating base;

you are required to be accessible for income earning duties and to undertake travel in response to emergency calls;

where you operate between two workplaces, one of which is your home.

In general, when you are on business travel, IRD will ignore minor incidental travel undertaken for private purposes, e.g. a minor detour to the dairy.

19.3.4 Car Parks

The IRD recently issued two public rulings (BR Pub 15/11 and BR Pub 15/12) to apply to an employer, and a group company of the employer, clarifying their interpretation of when the on-premises exemption applies to car parks. Inland Revenue considers parking as exempt from fringe benefit tax where the car park is on land owned or leased by the employer with exclusive use rights. In contrast, where the employer only holds a licence to occupy the car park and exclusive use cannot be established, FBT applies.

EXAMPLE

An employer arranges parking at a commercial car park for three of her employees. No particular spaces are designated for them, but the car park owner has an area reserved for pre-sold parking so that there are always three parks available for these employees. The Commissioner considers that “the premises of the employer” does not include the car park or any part of it. It does not form part of the employer’s premises as the employer does not own the car parks, and the car park owner has not parted with possession, but still retains control of the park.

Another distinguishing feature is the lack of specifically allocated parks. The requisite ownership or possessory interest is not, therefore, present for the car park to be called the “premises of the employer”. Accordingly, the provision of places at the car park by the employer to the employees is subject to FBT.

Summary

Casual parking arrangement - FBT

Assigned car parking spaces in a public building parking building, but no written lease agreement - FBT

Written lease agreement with designated car parks - No FBT

Employees use car parks owned by the employer - No FBT

19.3.5 Low Interest Loans

Where money is lent to an employee, either interest free or at a low rate of interest, then the difference between that rate and the prescribed rate of interest will be a fringe benefit. The prescribed rate is determined by the IRD and fluctuates in accordance with market rates. It is published every two months on the inside back cover of the FBA journals.

The definition of a loan includes any advance, deposit or money otherwise lent and includes a debit balance in the current account of a shareholder employee. However, the provision of normal trade credit by an employer to an employee is not subject to FBT. Also, loans in relation to employer share purchase schemes are exempt from FBT.

19.3.6 Tax Returns

An exemption from FBT is available where an employer provides an employee with assistance in the preparation of the tax return and that expenditure would have been deductible to the employee.

19.3.7 Non-Cash Benefits to Shareholder Employees

Where “other non-cash benefits” are granted to shareholder employees, employers have the option to treat the benefit as a fringe benefit or a dividend. “Other non-cash benefits” are a special class of fringe benefits. This class, which includes free or discounted goods, does not include low interest loans or the provision of motor vehicles. Where no election is made the benefit will be deemed to be a fringe benefit.

19.3.8 Subsidised or Free Goods and Services

Where the employer is in the business of manufacturing or producing goods, a fringe benefit will occur when the employee receives these goods at an amount that is less than the lowest price that would have been charged on an “arms length” basis. The value of the benefit is the lowest price charged by the employer in the open market at the time identical goods were provided to employees.

Where the employer is in the business of purchasing goods for resale, then a benefit occurs where the sale to the employee is less than the cost price paid by the employer.

There are two exemptions that apply to this second category, the first of which relates to goods that are on special. Where the goods are on special to the public and their normal retail price is $200 or less, and the goods are sold on normal staff discount, then no fringe benefit will arise so long as the price paid by the employee is greater than the lesser of:

95% of cost price to the employer; or

95% of the special price to the public

The second exemption applies if goods are not on special.

There will be no fringe benefits where these goods are sold to staff below cost, provided:

the goods are sold in the normal course of the employer’s business; and

the normal retail price of the goods is not greater than $200; and

the discount is the usual staff discount and is not greater than 5% of the price offered to the public

19.3.9 General exemption from FBT

Employers are entitled to a further exemption for “other fringe” including free gifts, rewards and prizes; and subsidised or discounted goods and services. The exemption is subject to certain thresholds as follows:

$300 of other benefits (see below) per employee per quarter for employers who file quarterly and $1,200 per employee per annum for annual filers; and

$22,500 of other fringe benefits for all employees per year.

If the threshold is exceeded then the full value of benefits is subject to FBT. i.e. The exemption is not deducted first.

Other benefits do not include low interest loans; use of motor vehicles; subsidised transport; contributions to a sick, accident or death fund; contributions to any specified insurance fund of a friendly society and any superannuation scheme.

There is an exemption from FBT for the private use of business tools that are provided primarily for business purposes and where the cost price of each tool does not exceed $5,000. For example, employees’ private use of cell phones and laptops will be exempt from FBT if the tool cost less than $5,000 and is primarily for business use.

19.4 Practical Hints

19.4.1 Motor Vehicle Exemptions

As noted in 19.3.3.1, a number of concessions are available for reducing the FBT payable on motor vehicles.

On any day which involves an emergency call, a day away for a business trip or travel between home and work where the motor vehicle constitutes a work related vehicle, no FBT is payable.

It is important that the employer maintains documentation to support the days on which FBT is not payable.

19.4.2 Motor Vehicle Record Keeping

An employer claiming any of the exemptions may elect to use a three-month test period to establish the FBT liability of a motor vehicle instead of keeping ongoing records of the number of days available for private use. In all exemption cases, the three month test period can be used to establish the exempt days per quarter or per annum for a period of three years.

During the test period, the employer must keep accurate records detailing the number of days the vehicle is available to the employee for private use or enjoyment. The three-month logbook concession does not extend to emergency calls and business days away.