Chapter 1 - New Zealand Tax Framework

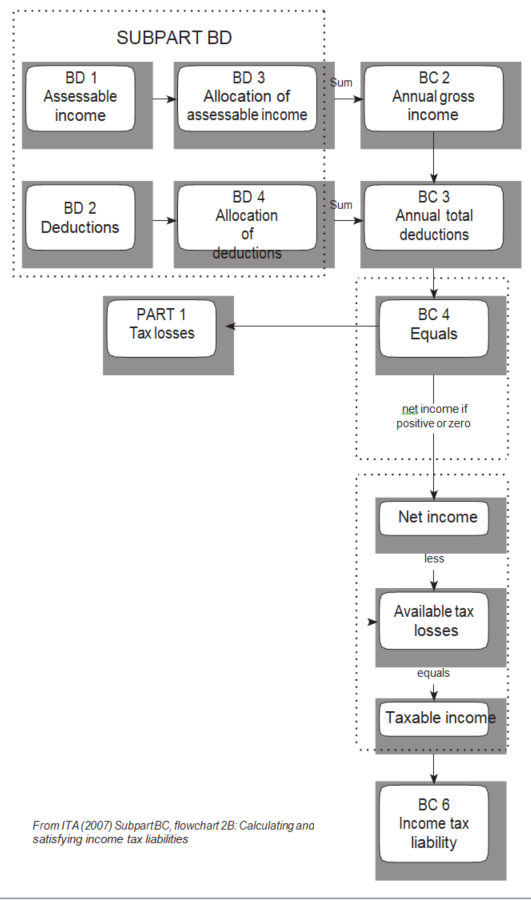

New Zealand taxation is imposed by the Income Tax Act 2007 (ITA). The basis for calculating tax is summarised in the following flowchart from the Core Provisions set out in Part B of the Act. This overview provides the context for details discussed in this quick reference guide.

“It’s income tax time again...: time to gather up those receipts, get out those tax forms sharpen up that pencil and stab yourself in the aorta.”

Dave Barry

(David McAlister Barry: Pulitzer Prize-winning author and columnist)

Calculating your income tax liability:

Step 1 - Determine Assessable Income

(References are to section in Subpart BD of the ITA)

Step 2 - Determine Taxable Income and Income Tax Liability

Comments / explanation:

Allocate income and deductions to the correct tax year (referred to in the Act as “income year”).

Gross Income minus deductions equals net income if the answer is positive, and net loss if the answer is negative.

Tax losses carried forward from previous years may be set off against net income from the current year to reduce the taxable income. A net loss in the current year may be added to previous tax losses increasing the amount that may be carried forward to set off against future net income.

Multiply taxable income by the basic tax rate to calculate your tax liability. If the result is negative, the tax to pay is zero.

“Taxation according to income is the most effective instrument yet devised to obtain just contribution from those best able to bear it and to avoid placing onerous burdens upon the mass of our people.”

Franklin Roosevelt

Step 3 - Satisfying your Income Tax Liability

Any tax credits that you may have must be used to satisfy your tax liability for a tax year as far as the credits extend. If the credits exceed the tax liability, the Act sets out the order in which the credits must be used (s LA 4).

This guide clarifies the details of calculating income tax and meeting your tax liabilities. It also covers Goods and Services Tax (GST), Fringe Benefit Tax (FBT), Accident Compensation (ACC) payments, as well as tips, traps and practical advice to help you minimise the tax that you pay, while meeting your compliance requirements. It all starts with effective tax planning.