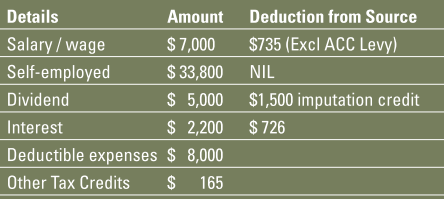

Appendix – Tax Facts – A Brief Summary

The information contained in this appendix is subject to change. Check our IRD Update page for changes.

A1.1 Individual Rates

A1.2 Companies

A1.3 Trusts

A2 Use of Money Interest

A3 Entertainment Expenditure

A4 Fringe Benefit Tax (FBT)

A4.1 FBT Rates

A4.2 Return & Payment Dates

A4.3 Fringe Benefit Value of Motor Vehicles

A4.4 Low or Interest Free Loans

A5 Goods & Services Tax (GST)

A6 Motor Vehicle Reimbursement Allowances

A7 Depreciation

A8 Dividends

A9 KiwiSaver

A10 Non-Resident Withholding Tax Rates

A11 Income Tax Payment Dates

A12 PAYE Electronic Filing

A13 Resident Withholding Tax Rates

A14 Proposed ACC Earner Levy

A1 Income Tax Rates

A1.1 Individual Rates

Independent tax earner’s credit for taxable incomes of

$24,000-$48,000. Available if you:

have an annual income between $24,000 and $48,000 for the tax year;

are tax resident in New Zealand;

do not receive an income tested benefit, a Veteran’s Pension, New Zealand Superannuation, or overseas equivalent; and

neither personally nor a partner is entitled to working for families tax credits, or is receiving an overseas equivalent

The credit is $520 ($10 per week) for an income of $24,000 to $44,000. If you are eligible but earn over $44,000, your annual entitlement to IETC decreases by 13 cents for every additional dollar earned up to $48,000.

A1.2 Companies

28% for resident & non-resident companies.

A1.3 Trusts

Trustee income taxed at 33%

Beneficiary income taxed at beneficiary’s marginal tax rate, except distributions to minors (under 16 years of age) which are taxed at the trustee rate of 33% (excluding distributions to minors of $1,000 or less).

A2 Use of Money Interest

Use of money interest is paid by the IRD on overpayments of tax and is charged by the IRD on underpayments of tax. The rates vary and were updated with effect from 29 August 2019:

8.35% on underpayments of tax (deductible)

0.81% on overpayments of tax (assessable)

Further updates will be reflected here.

A3 Entertainment Expenditure

Certain categories of entertainment expenditure are only 50% deductible. These include:

Corporate boxes

Holiday accommodation

Yachts and other pleasure craft

Food and beverages provided:

At any of the above, or

Off the premises of the taxpayer (e.g. business lunch), or

On the premises of the taxpayer at a social function

There are a number of exceptions from these rules. The 50% add back is subject to an annual GST adjustment.

A4 Fringe Benefit Tax (FBT)

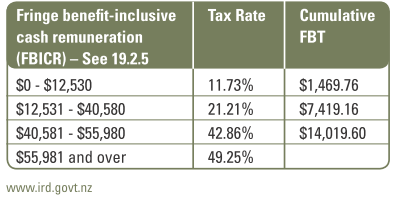

A4.1 FBT Rates

Attributed benefits rates using the alternate rate system - applied to Fringe benefit-inclusive cash remuneration (FBICR):

Motor vehicles and loans, plus other categories of benefits exceeding $1,000 by category, must be attributed. Benefits that cannot be attributed are generally taxed at 42.86%. 49.25% applies for FBT received as a shareholder- employee (or associate) with 10% or more shareholding in the employer company.

General exemption for ‘other benefits’: $300 per employee per quarter with total benefits for all employees not to exceed $22,500pa.

A4.2 Return & Payment Dates

A4.3 Fringe Benefit Value of Motor Vehicles

5% per quarter of original cost (GST inclusive) of vehicle 20% of cost if the FBT return is filed on an annual basis

A4.4 Low or Interest Free Loans

Benchmark interest rate varies and is reviewed quarterly. For current rates at any point in time refer here.

A5 Goods & Services Tax (GST)

Standard rate: 15%

Exported goods and services: 0%

Supplies exempt from GST include:

Financial services

Residential rental income

Wages/salaries and most directors’ fees

A6 Motor Vehicle Reimbursement Allowances

Several options are available. See 26.4.5. The IRD is implementing a new 2-tiered Kilometre Rate Method for establishing reimbursement rates for employees who use private vehicles for work purposes. These rates will also be available to the self-employed who can use them to claim business costs of using their motor vehicles. The 5,000 km limit will no longer apply.

A7 Depreciation

Depreciation is calculated based on IRD approved economic rates. The IRD has a rate finder on its website (www.ird.govt.nz). Either the straight line or diminished value method can be used.

Low value assets (costing $500 or less) can be written off in the year acquired.

A8 Dividends

Dividends are taxed at a flat RWT rate of 33% of gross dividends (less imputation credits).

Dividends from a listed PIE are not liable for RWT.

A9 KiwiSaver

Employees and employers each contribute 3% or more of the member employee’s gross pay.

Members are entitled to up to $10 tax credit per week as a government subsidy.

All employer contributions are subject to employer superannuation contribution tax (ESCT)

A10 Non-Resident Withholding Tax Rates

*The rate is normally 0% if fully imputed dividends are paid subject to double tax agreement.

The rate of NRWT on interest is zero if the Approved Issuer Levy of 2% has been paid.

A11 Income Tax Payment Dates

A12 PAYE Electronic Filing

Large employers must file their Employer Monthly Schedule (IR348) electronically. (See option also for Payday filing for PAYE in 26.4.3).

Employers with fewer than 50 employees may qualify for an exemption.

A13 Resident Withholding Tax Rates

Interest

A14 Proposed ACC Earner Levy